This 232-Day Stretch Has Delivered Gains in 10 of 10 Years for Apple Inc. (AAPL)

Apple Inc. is pulling back from record territory just as it approaches a long seasonal window that has delivered gains every year for a decade, setting up a key test of the stock’s AI-fueled growth story.

Key takeaways

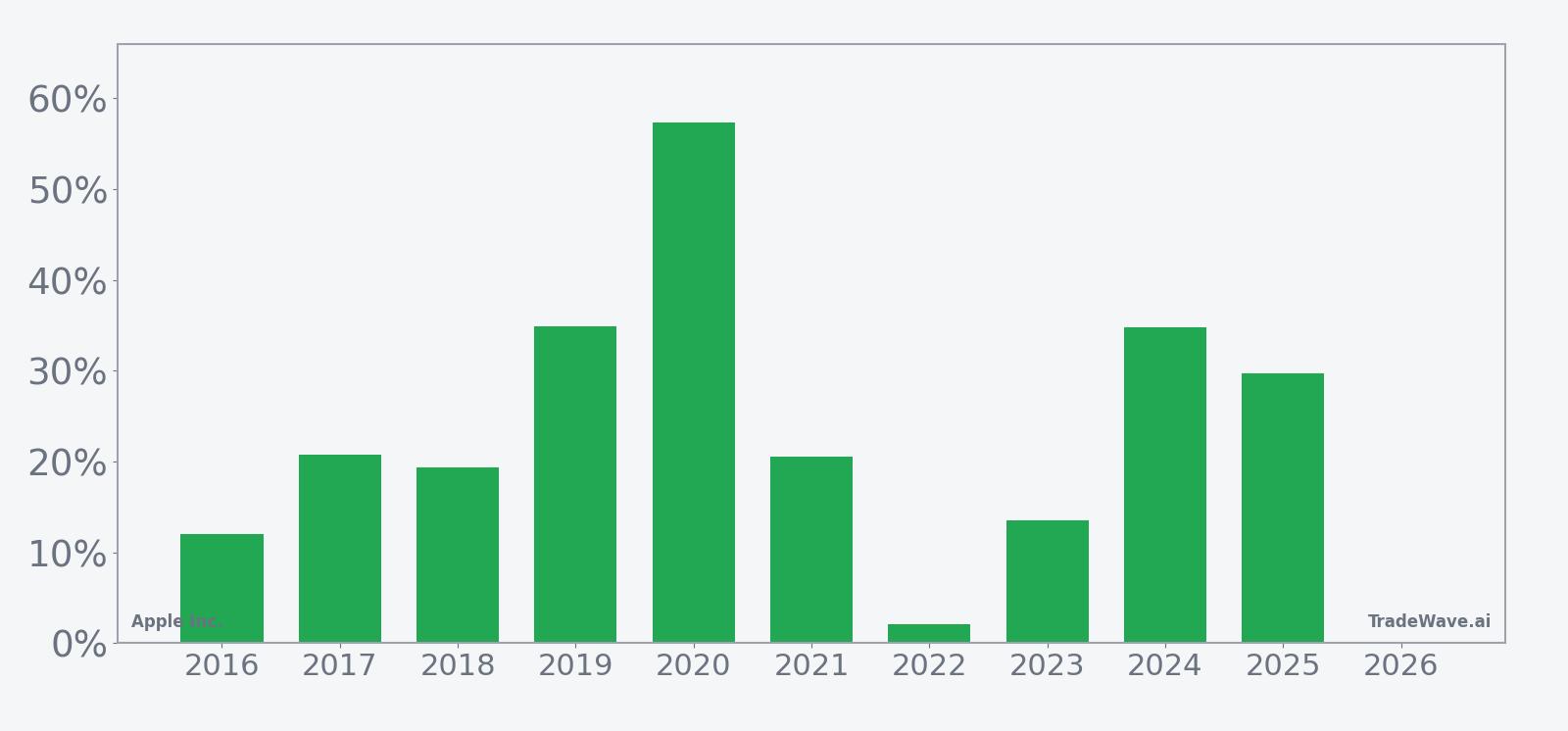

- A 232-day seasonal window for Apple Inc. starting Mar 13 has produced gains in 10 of 10 years, a 100% win rate for a long bias.

- Average profit across those years is 24.51%, with cumulative gains of 737% over the decade-long sample.

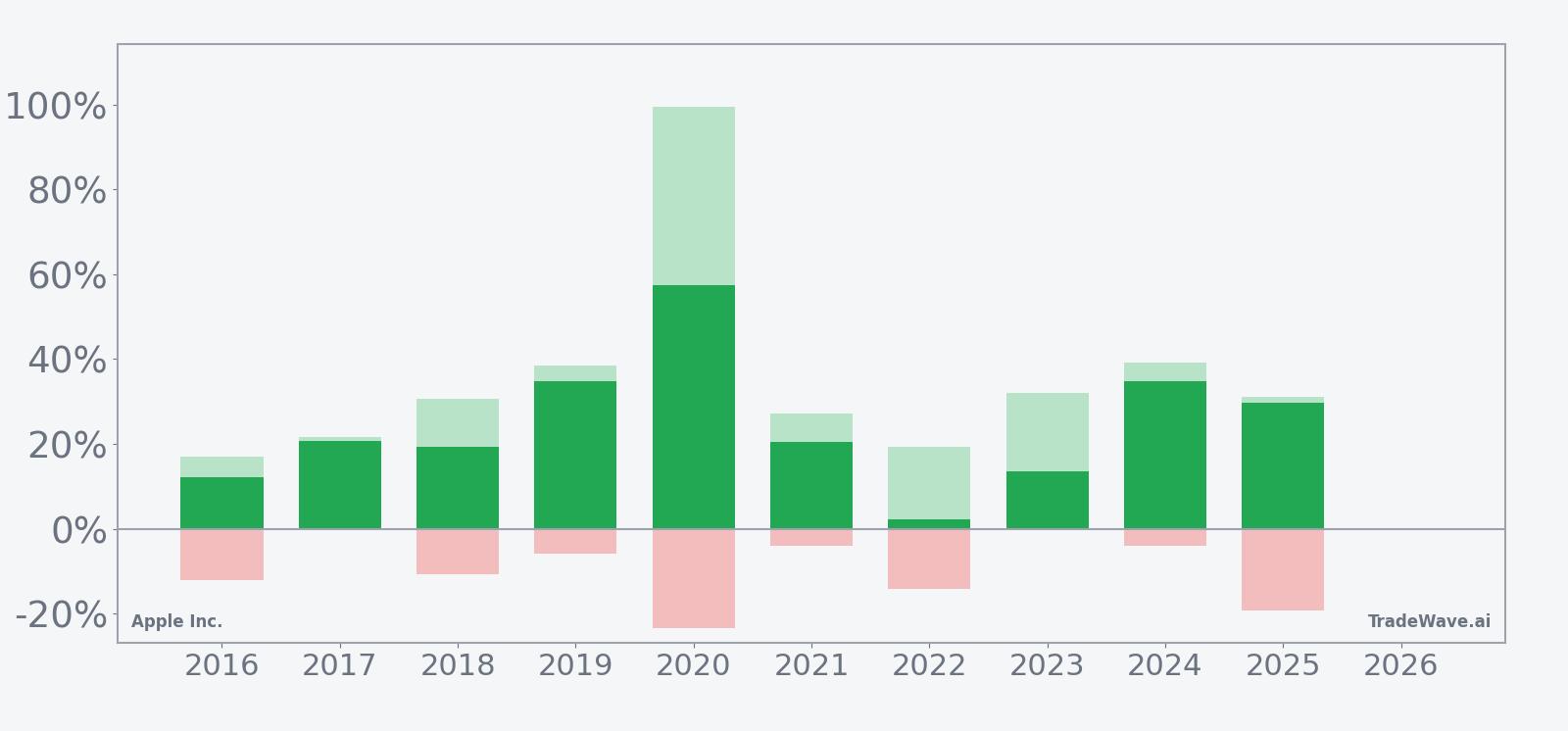

- Intraperiod swings have been large: the best point-to-peak move reached 99.45% in 2020, while the worst drawdown hit -23.51% that same year.

- Today AAPL closed at $264.18, about 8.3% below its 52-week high of $288.08, after sliding 3.2% on the day.[1]

- Apple is guiding for 13% to 16% revenue growth in the March quarter on strong iPhone demand, reinforcing a growth backdrop heading into the window.[1]

- Recent commentary from Wedbush frames 2026 as Apple’s “year of AI,” adding another narrative tailwind if the historical pattern repeats.[13]

According to historical data from TradeWave.ai, this upcoming stretch for Apple has behaved very differently from an average year, with a distinct long-biased regime that has repeated across the past decade.

Seasonal window

Apple Inc. has risen in 10 of 10 years during this 232-day window, averaging 24.51% gains for a long setup. The next iteration begins on Mar 13, with the stock currently at $264.18 and trading about 8.3% below its 52-week high of $288.08.[1] That combination of a clean pullback from highs and a historically powerful window is why this stretch is on traders’ calendars.

Across the 10-year sample, the pattern is straightforward: every single iteration has finished higher, with cumulative gains of 737% when you stack the windows back to back. Average winners gained 24.51%, and the median outcome of 20.63% shows that the typical year has delivered a solid double-digit move rather than being skewed by one outlier.

The strongest year in the sample was 2020, when Apple’s net return in the window reached 57.36% after a maximum favorable move of 99.45% from the entry, even as the worst drawdown inside that same stretch hit -23.51%. At the other end of the spectrum, 2022 barely cleared the bar with a 2.1% net gain, but even that “soft” year saw a point-to-peak rally of 19.25% before a -14.2% intraperiod slide.

The historical seasonal average shows gains building gradually rather than in a single burst, with strength skewed toward the middle and later portions of the window. Early weeks have often been choppy, which lines up with the fact that several years saw meaningful drawdowns before the trend kicked in.

A stacked view of yearly net returns alongside peak rallies and worst drawdowns shows how much room Apple has historically had to run, and how deep the air pockets can be along the way.

The maximum favorable moves in most years sit well above the final net gains, which means Apple has often overshot to the upside inside the window before settling back. At the same time, maximum adverse moves in the low double digits are common, underscoring that even in a 100% win-rate sample, the path has rarely been smooth.

History does not guarantee future results; adverse excursions can be large even in winning windows, and traders need to respect the drawdown profile as much as the upside record.

Price and near-term drivers

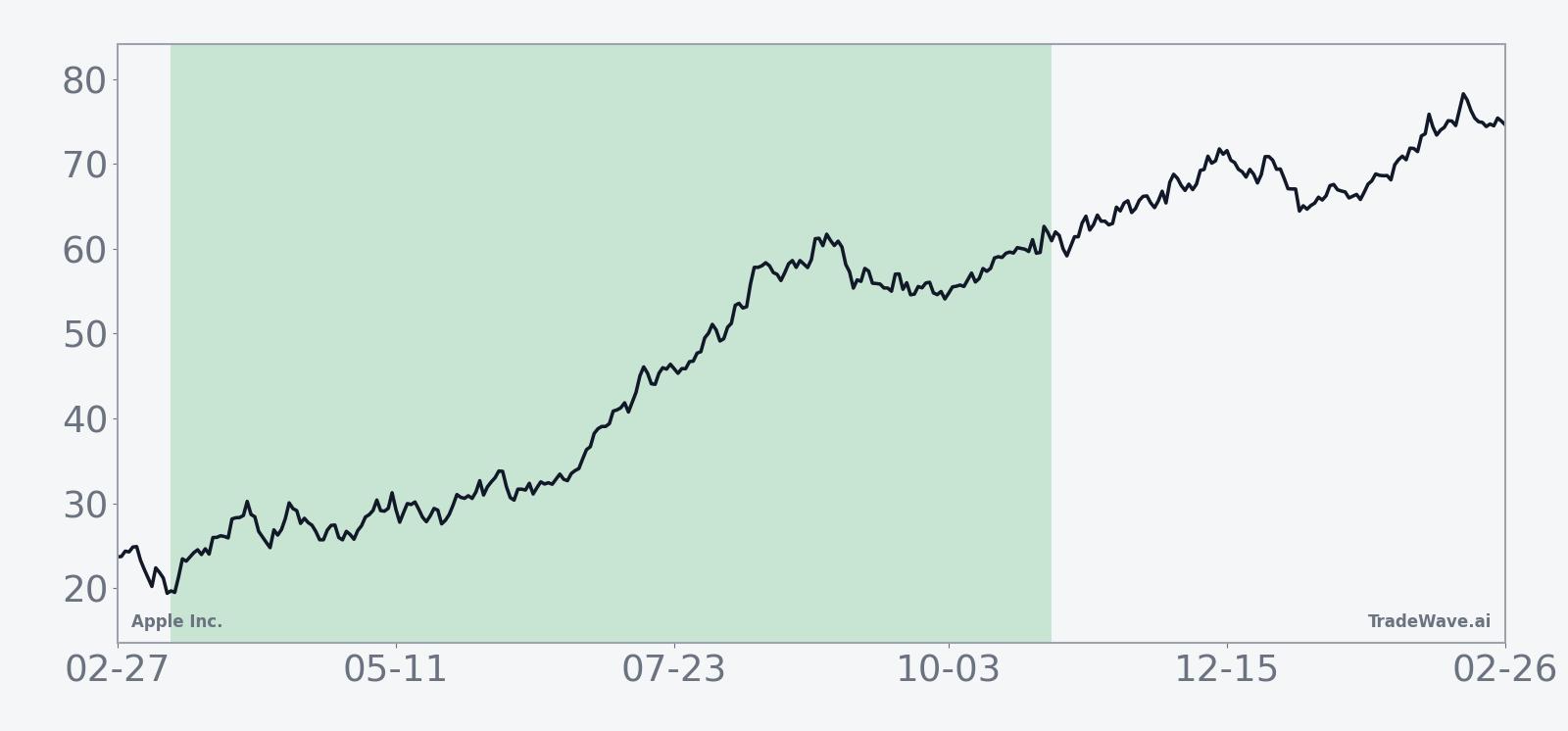

Apple shares fell 3.2% on Monday to close at $264.18, leaving the stock about 8.3% below its 52-week high of $288.08 and still comfortably above its 52-week low of $167.74.[1] The pullback follows a powerful run that helped push Apple’s market value to the $4 trillion mark in late 2025, cementing its role as a key driver of major equity indices.[4]

The near-term fundamental backdrop is unusually strong heading into this seasonal stretch. On Jan 29, Apple projected 13% to 16% revenue growth for the March quarter, citing robust iPhone demand and record March-quarter expectations.[1] That guidance builds on a string of beats in 2025, including July-quarter revenue of $94.04 billion that topped estimates by nearly $5 billion and highlighted the resilience of both hardware and services.[2][3]

Analysts remain broadly constructive. Wedbush keeps a Buy stance with a $290 price target, framing Apple as a core AI beneficiary and calling 2026 the company’s “year of AI” as investors look for more on-device intelligence and cloud integration.[11][13] That target sits only modestly above the current price, reflecting how much optimism is already embedded after last year’s rally, but it also signals that the Street is not treating the latest dip as the start of a structural breakdown.

There are risks on the radar. In Aug 2025, a former Louisiana attorney general launched an investigation into Apple’s officers and directors, adding a legal overhang that investors have had to discount alongside regulatory scrutiny elsewhere in Big Tech.[12] Options-focused commentary in late 2025 also flagged how quickly post-earnings pops in Apple can fade, a reminder that even strong fundamental stories can see sharp short-term reversals.[9][10]

The chart below situates the latest pullback against Apple’s broader uptrend over the past year.

Earnings and guidance context

Apple’s most recent detailed outlook came with its late-January update, when management guided to 13% to 16% revenue growth for the March quarter on the back of strong iPhone demand and continued services expansion.[1] That follows a July 2025 quarter where revenue hit $94.04 billion versus expectations of $89.54 billion, with earnings per share of $1.57 beating the $1.43 consensus and services revenue reaching record levels.[2][3][6]

Across 2025, Apple consistently leaned on its installed base and services ecosystem to smooth hardware cycles. The May 2025 earnings call highlighted a 5% year-over-year revenue increase to $95.4 billion and record services revenue, reinforcing the narrative that Apple is less dependent on any single iPhone cycle than in the past.[6] That diversification matters heading into a long seasonal window, because it reduces the odds that one product miss derails the entire stretch.

Looking ahead, investors are focused on how quickly AI features can translate into incremental revenue. Commentary in mid-2025 framed upcoming iPhone iterations and AI capabilities as key swing factors for growth, with Wedbush expecting “good headline numbers” and emphasizing the importance of the iPhone 17 cycle.[11] If Apple can pair that product cadence with the historically strong seasonal regime that starts in mid-March, the earnings narrative and the calendar could be pulling in the same direction.

Macro and sector backdrop

Apple’s seasonal window does not exist in a vacuum. As one of the largest weights in major U.S. equity indices, its behavior often tracks broader risk appetite and macro conditions. In July 2025, for example, Apple’s revenue beat and upbeat iPhone commentary came against a backdrop of resilient consumer spending and ongoing enthusiasm for mega-cap tech, helping pull the wider market higher.[2][3]

By late 2025, the conversation had shifted toward how much of that optimism was already priced in. Coverage around Apple’s $4 trillion market cap milestone stressed that expectations for AI, services and hardware refresh cycles were elevated, which can amplify volatility when macro data or policy surprises hit.[4][5] The upcoming 232-day window will unfold across multiple Fed meetings and data prints, so traders will be watching whether Apple continues to trade as a high-beta proxy for tech sentiment or decouples based on its own fundamentals.

Valuation and positioning

Valuation is not cheap, but it has not stopped Apple from delivering strong seasonal runs in the past. Analysis in late 2025 argued that Apple’s surging free cash flow left the stock as much as 20% undervalued, even after the move to record highs, pointing to buybacks and capital returns as key supports.[5] At the same time, options strategists highlighted how crowded positioning can make post-earnings swings more violent, especially when the stock is near records.[9][10]

Today’s pullback leaves Apple trading just below its 50-day moving average of roughly $265.02, with 20-day average volume around 54 million shares, suggesting liquidity remains deep even as short-term momentum cools.[1] That sets up a classic tension heading into the seasonal window: a stock that is still priced for growth, but no longer stretched at the absolute highs, with a decade-long record of strong performance in this specific slice of the calendar.

What to watch as the window opens

The next few weeks will determine whether Apple leans into its historical pattern or breaks it. The first checkpoint is price action around the Mar 13 start date: traders will watch whether the stock can reclaim and hold above the 50-day moving average and then make a sustained push back toward the $288 area that marked the 52-week high.[1]

Earnings and product news will be the second pillar. The March-quarter results tied to Apple’s 13% to 16% growth guidance will land inside the early part of the window, and any update on AI features or iPhone demand will shape how much fuel the seasonal regime has to work with.[1][11][13] Strong numbers that confirm the growth story would align cleanly with the long-biased history of this stretch.

Volatility inside the window will be just as important as direction. Historically, even winning years have seen double-digit drawdowns, so traders will be watching how deep any pullbacks run relative to past maximum adverse moves. A pattern of shallow dips and strong rebounds would look like prior strong years such as 2019 and 2024, while a deeper air pocket more in line with 2020 or 2022 would test conviction.

Finally, watch how Apple trades around macro events and sector rotations. As a $4 trillion bellwether with a Buy-rated AI narrative, its behavior in this 232-day stretch will feed directly into broader tech and index sentiment.[4][5][13] If the stock can once again turn this window into a sustained advance, it will reinforce the idea that Apple’s calendar sweet spot remains intact; if not, the break in a 10-for-10 record will be a story in its own right.

Sources

- [1] Seeking Alpha – Apple projects 13%-16% revenue growth for March quarter as iPhone demand drives record results (Jan 30, 2026)

- [2] Reuters – Apple revenue forecast beats estimates as iPhone sales soar (Jul 31, 2025)

- [3] Seeking Alpha – Apple Q3 revenue crushes estimates by nearly $5B, shares edge higher (Jul 31, 2025)

- [4] Business Insider – Apple is reporting earnings today after reaching a historic $4 trillion market cap (Oct 30, 2025)

- [5] Barchart – Apple’s Free Cash Flow Surges, Implying AAPL Stock Could Be 20% Too Cheap (Nov 2, 2025)

- [6] Yahoo Finance – Q2 2025 Apple Inc Earnings Call (May 2, 2025)

- [9] MarketWatch – With Apple stock near a record high as earnings loom, here’s the options trade to make (Oct 20, 2025)

- [10] CNBC – Apple gave up its earnings pop. How to trade it from here (Oct 31, 2025)

- [11] Seeking Alpha – Apple expected to report 'good headline numbers' says Wedbush (Jul 30, 2025)

- [12] Morningstar – Apple investigation initiated by former Louisiana attorney general (Aug 16, 2025)

- [13] Seeking Alpha – Apple sell-off 'unwarranted,' as Wedbush says 2026 is the tech giant's year of AI (Feb 17, 2026)