High Mortgage Rates and Weak Housing Turnover Pressure Big-Project Demand at Home Depot (The) (HD)

Home Depot (The) is down for 2026 but approaching a long seasonal stretch that has historically favored the bulls, giving investors a structured backdrop as housing and consumer trends remain in flux.

Key takeaways

- Home Depot (The) enters a 326-day seasonal window starting Mar 13 that has historically been strongly bullish for long positions.

- Across the past 15 years, the pattern has been profitable in 100% of cases, with 15 winners and 0 losers.

- Average profit in winning years has been 21.39%, with a median gain of 24.02% over the window.

- The TradeWave Ratio of 1.94 suggests price has typically traveled meaningfully in the trade direction within the window, beyond just the final close.

- Historical best and worst intraperiod moves show sizable rallies but also notable drawdowns before gains, underscoring the need to manage volatility.

- The setup arrives as the stock is down about 8.0% year to date and digesting mixed signals from housing and professional demand.

According to historical data from TradeWave.ai, the coming months line up with one of Home Depot (The)’s most distinctive long-term seasonal regimes, offering a quantitative backdrop to the stock’s fundamental story.

Seasonal window

This seasonal window begins on Mar 13, 2026 and spans 326 trading days. Today the stock trades at $375.09, down about 8.0% for 2026 so far, leaving it in a consolidation phase after a strong multi-year run.[4]

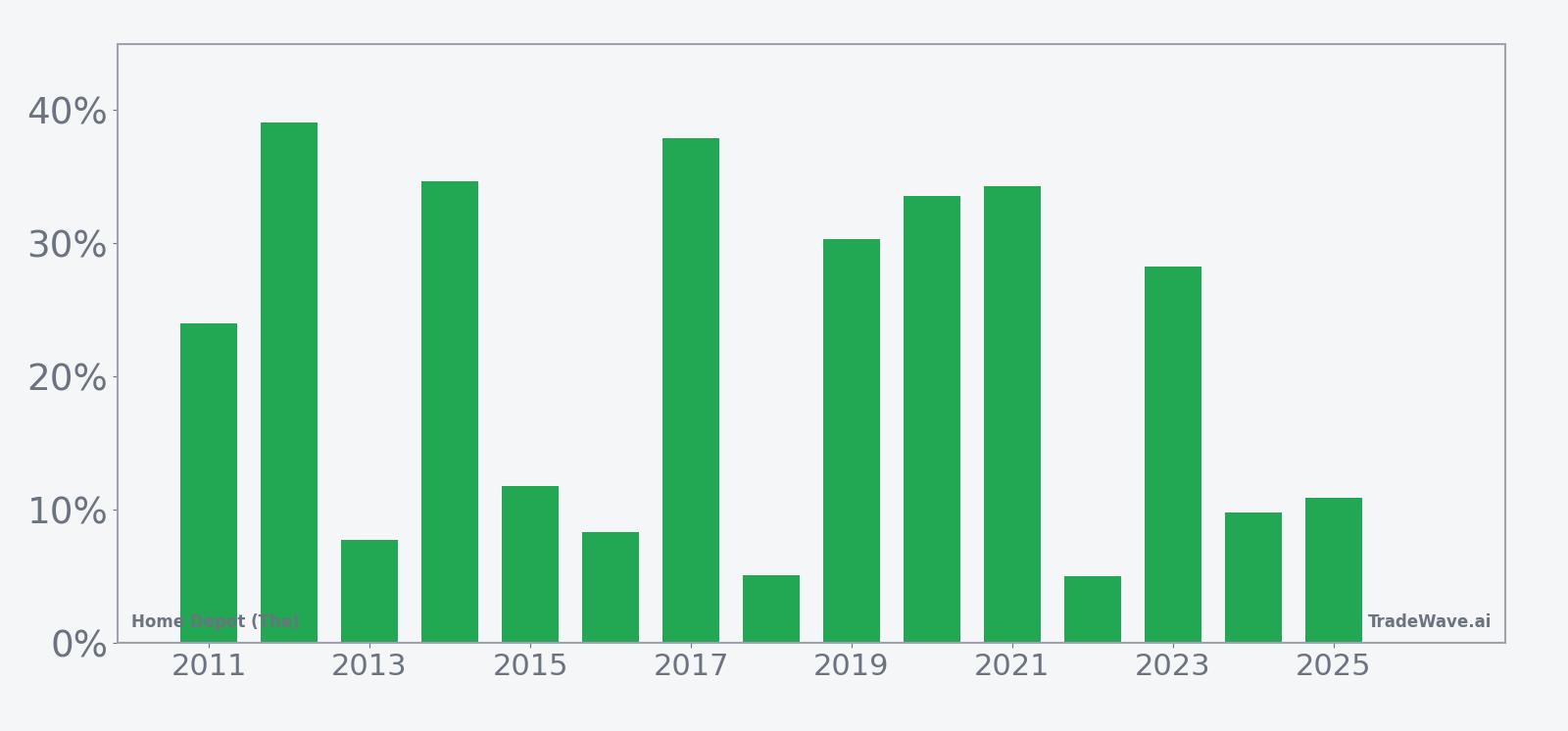

Historically, this has been a long-biased pattern: the trade direction is long, and all 15 years in the sample ended the window with positive returns. The average profit of 21.39% and median gain of 24.02% suggest that in a typical year, the stock has added roughly a fifth to a quarter of its value over this stretch, although individual outcomes have varied.

The per-year table shows that some of the strongest seasons came in 2017 and 2021, when Home Depot (The) logged net gains of 37.88% and 34.29% respectively, while even softer years such as 2016 and 2018 still finished with single-digit advances. In 2020, the stock delivered a 33.52% net gain over the window, but that year also featured one of the deepest intraperiod drawdowns, highlighting how volatile the path can be even in a winning season.

The 15-year average trend line suggests that gains have tended to build steadily through the window rather than arriving in a single burst. There are periods of consolidation and pullback, but the typical pattern shows a gradual climb, with momentum often strengthening in the middle and later portions of the regime.

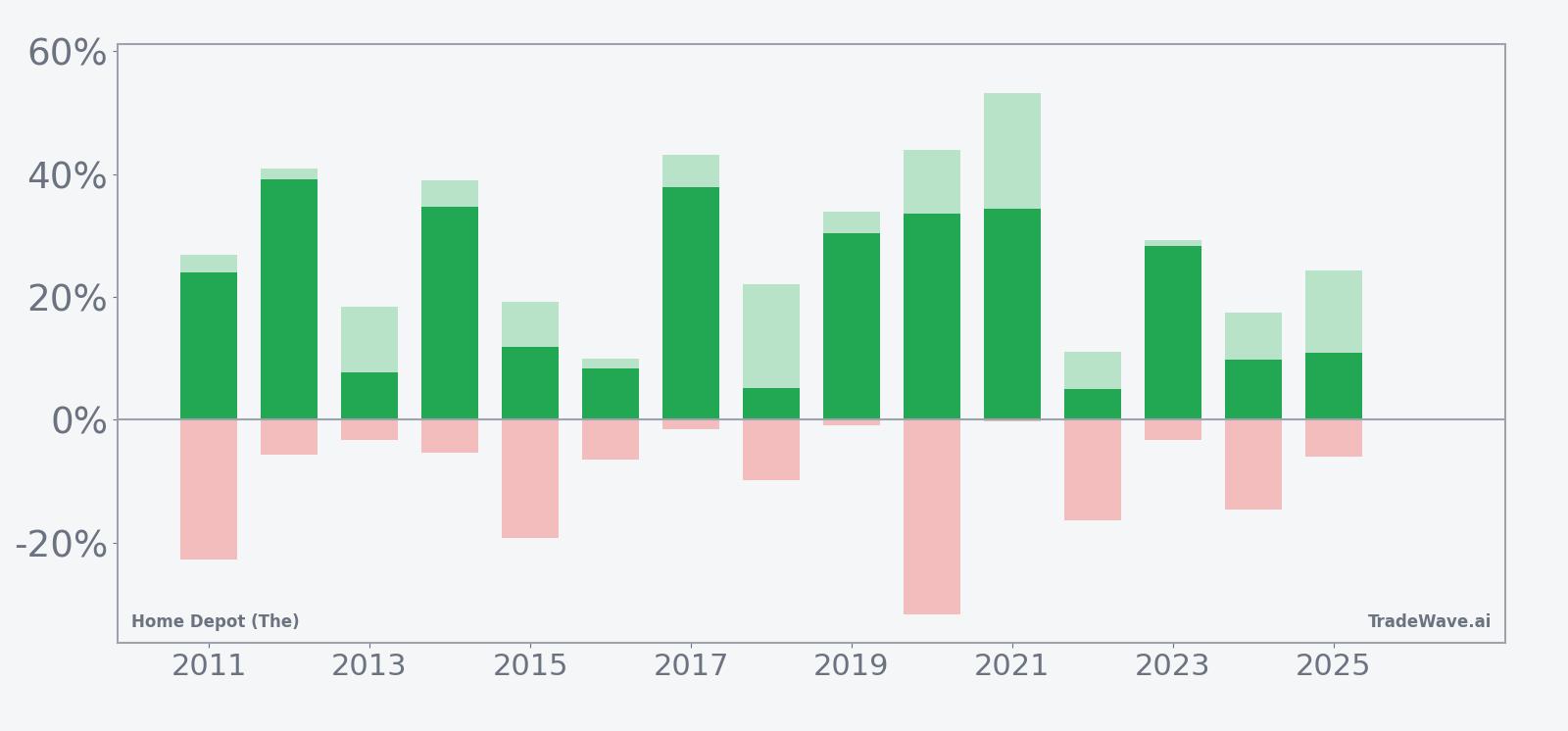

A combined view of yearly net results and intraperiod swings helps clarify how upside and downside have interacted in this window.

The combined net, peak favorable move and worst drawdown chart shows that in strong years such as 2021, the maximum favorable move reached more than 50%, while the worst adverse move was very limited, indicating a relatively smooth climb. By contrast, 2020 featured a maximum favorable move of 43.9% but also a worst adverse move of -31.62%, meaning the stock experienced a deep drawdown at some point before finishing higher. Across the sample, maximum favorable moves have generally been larger than maximum adverse moves, but the latter can still be significant, particularly in years like 2018 and 2022 where intraperiod downside reached double digits before the pattern recovered.

The cumulative return profile, with a cumulative gain of 1,584% across the 15-year history and an annualized return of 20.72%, underscores how consistently this window has contributed to long-term performance when viewed as a repeated seasonal regime. Taken together, the historical pattern defines the quantitative seasonal backdrop for the coming period.

History does not guarantee future results; adverse excursions (MAE) can be large even in winning windows.

Price and near-term drivers

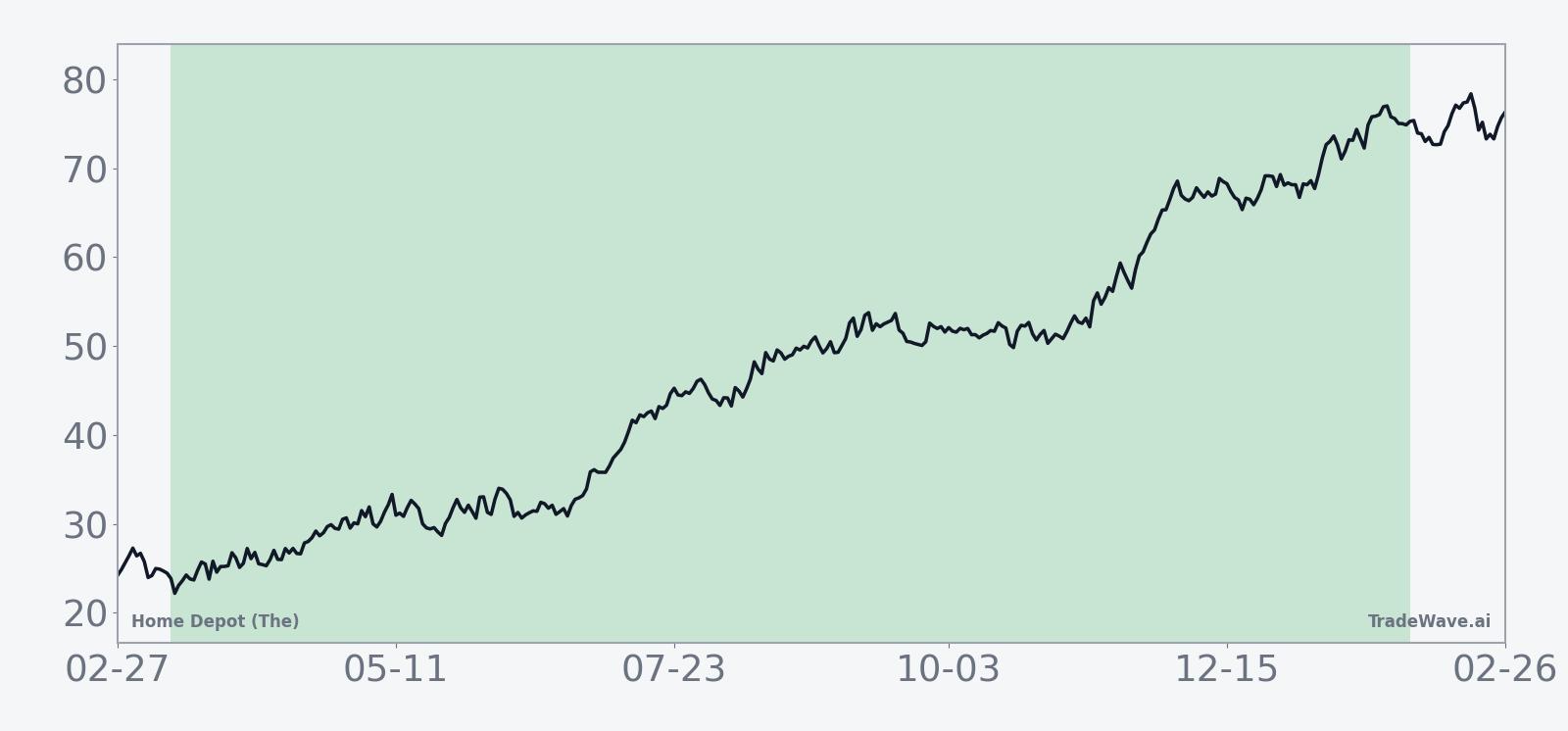

Home Depot (The) shares closed at $375.09 on Feb 27, down 0.13% on the day and about 8.0% lower year to date as investors reassess the outlook for housing-related spending and big-ticket projects.[4] The stock has been consolidating after a strong multi-year advance, with traders weighing how quickly demand can reaccelerate if borrowing costs ease.

The chart below situates the latest move in its recent multi-month context.

The latest fundamental check-in came on Feb 24, when Home Depot reported fourth-quarter 2025 results that topped expectations on earnings and showed a modest return to positive same-store sales growth.[4] Adjusted earnings per share of $2.72 beat estimates of $2.54, and comparable sales rose 0.4% against forecasts for flat performance, while management reiterated its fiscal 2026 outlook, signaling confidence that demand from professional customers and core home improvement projects can support modest growth.

Those results followed a more challenging third quarter in November 2025, when the company missed earnings expectations and trimmed its full-year outlook as high mortgage rates and a softer labor market weighed on large-scale renovation projects.[1][3] At that time, management pointed to consumers delaying discretionary home improvement spending, particularly on big-ticket items, and guided to slower sales growth and a steeper decline in adjusted earnings for fiscal 2025.

Macro conditions remain a key swing factor. Elevated interest rates and high mortgage costs are reducing housing turnover, which historically has been a driver of demand for remodeling and repair, while housing affordability sits near multi-decade lows as limited supply and higher financing costs squeeze buyers.[1][2] That backdrop has pressured do-it-yourself spending but has also encouraged Home Depot to lean more heavily on professional customers such as contractors and tradespeople, where demand has been more resilient.[2][11]

Strategically, the company is investing in technology and services aimed at those professional customers, including an AI-powered push to improve ordering, inventory and project management for contractors.[10] Analysts covering the stock maintain a broadly positive stance, with CNBC’s Investing Club citing Home Depot as a favored way to play the potential for lower interest rates over time, and a consensus price target around $420 implying upside from current levels if the company can execute on its growth plans.[2][10]

Investor sentiment has also been shaped by governance and reputational considerations. In January 2026, some shareholders raised questions about how law enforcement agencies use data from Home Depot’s surveillance systems, highlighting the broader scrutiny large retailers face around privacy and corporate responsibility.[14] While not directly tied to near-term earnings, such debates can influence how certain investors view risk and long-term positioning in the name.

Earnings and guidance context

Across its most recent two quarters, Home Depot (The) has delivered a mixed but stabilizing earnings picture. In the third quarter of 2025, revenue of $41.35 billion slightly beat expectations, but adjusted EPS of $3.74 fell short of the $3.84 consensus, and management cut its full-year outlook as consumers pulled back on discretionary projects.[1][3] By the fourth quarter, the company had returned to beating earnings estimates and posted a small positive surprise on same-store sales, suggesting that the worst of the demand slowdown may be passing even if growth remains modest.[4]

For fiscal 2025, management expects sales growth of about 2.8%, with comparable sales only slightly positive and adjusted EPS declining by roughly 5%, a steeper drop than the 2% decline previously forecast.[1][3] Looking ahead to fiscal 2026, the company is guiding to sales growth of 2.5% to 4.5%, flat to 2% comparable sales growth and adjusted EPS that is flat to up 4%, a profile that points to gradual improvement rather than a rapid rebound.

Street expectations broadly align with that cautious optimism. Analysts see Home Depot as well positioned to benefit if interest rates ease and housing activity picks up, but they also acknowledge that the timing and magnitude of any recovery in big-ticket spending remain uncertain.[2][7] That tension between a still-sluggish macro backdrop and a historically strong seasonal window is likely to shape how investors interpret upcoming quarterly results once the next earnings date is set.

Macro and sector backdrop

Home Depot (The) sits at the intersection of consumer spending, housing and construction, making it particularly sensitive to interest rates and labor market trends. Elevated borrowing costs have cooled home sales and refinancing activity, which in turn has reduced the churn that often drives renovation and repair projects.[1][2] At the same time, a tight housing supply and affordability constraints have encouraged some homeowners to stay put and invest in their existing properties, supporting a baseline level of demand.

Within the home improvement retail sector, Home Depot has been leaning into its professional customer base to offset softer do-it-yourself traffic.[2][11] Surveys of contractors and tradespeople in 2025 indicated that many felt reasonably confident about their pipelines, an encouraging sign for demand in categories such as building materials, tools and rental equipment that skew toward professional users.[11] The company’s investments in digital tools, supply chain and job-site delivery are aimed at deepening those relationships and capturing a larger share of wallet from pros.

Consumer-facing peers and broader retail benchmarks have also been contending with shifting spending patterns as households balance higher debt service costs with wage gains and accumulated savings.[6][8] In that environment, investors have tended to reward companies that can demonstrate pricing power, cost discipline and targeted growth initiatives, while punishing those that rely heavily on discretionary big-ticket purchases.

Valuation and positioning into the window

With the stock down about 8.0% year to date and trading below the consensus price target of $420, Home Depot (The) is entering its historically strong seasonal window from a position of consolidation rather than euphoria.[2][4] That starting point may matter for how investors interpret the seasonal statistics: a long regime that has historically delivered double-digit average gains could be viewed differently when the stock is already extended versus when it is digesting prior advances.

Analysts continue to rate the shares positively, citing the company’s scale, professional focus and potential leverage to any eventual easing in interest rates.[2][10] At the same time, the guidance for only modest sales and earnings growth over the next two fiscal years underscores that the fundamental story is one of gradual normalization rather than a sharp cyclical snapback.[1][7] For investors, the seasonal pattern provides one more lens through which to frame that trade-off between near-term macro headwinds and longer-term structural strengths.

What to watch as the seasonal window opens

As the 326-day seasonal window beginning Mar 13 approaches, investors will be watching several key signposts. First, any updates on housing activity, mortgage rates and affordability will be critical for gauging whether the macro drag on big-ticket projects is easing or persisting.[1][2] A sustained improvement in home sales or refinancing could support the kind of steady demand backdrop that has historically aligned with stronger seasonal performance.

Second, the next earnings update and any interim commentary from management will be scrutinized for signs that comparable sales are tracking toward the upper or lower ends of guidance ranges.[4][7] Evidence that professional demand remains firm and that do-it-yourself spending is stabilizing would fit more comfortably with the long-biased seasonal pattern, while renewed pressure on comps or margins could test investor patience even in a historically favorable window.

Third, price action around key technical levels will matter. With the stock consolidating below analyst targets, traders will be looking to see whether pullbacks into the window resemble the deeper intraperiod drawdowns seen in years like 2018, 2020 and 2022, or whether downside remains more contained as in 2017 and 2021. How the stock behaves during bouts of volatility will help determine whether the historical tendency toward strong net gains reasserts itself.

Finally, broader sentiment toward consumer and retail names, including flows into and out of sector ETFs, will shape how much room investors are willing to give Home Depot (The) as it moves through this long seasonal regime.[6][8] If the stock can pair even modest fundamental improvement with the kind of steady, seasonally aligned trend seen in many prior years, the upcoming window could again play an outsized role in its multi-year return profile. If not, the historical pattern will serve as a reminder that even strong seasonal tendencies can be overwhelmed by shifts in the macro and earnings landscape.

Sources

- [1] CNBC, “Home Depot will report earnings before the bell. Here's what to expect” (Nov 18, 2025)

- [2] CNBC, “Despite a tough quarter, Home Depot remains the best stock play on lower rates” (Nov 18, 2025)

- [3] Yahoo Finance, “Home Depot stock falls after company cuts full-year outlook” (Nov 18, 2025)

- [4] Reuters, “Home Depot beats quarterly sales estimates on demand from professional customers” (Feb 24, 2026)

- [5] CNBC, “Stocks making the biggest moves premarket: Home Depot, Blue Owl Capital, Amer Sports & more” (Nov 18, 2025)

- [6] Yahoo Finance, “What To Expect in the Markets This Week” (May 18, 2025)

- [7] The Wall Street Journal, “Home Depot Shares Fall as Retailer Gives Guarded Fiscal 2026 Forecast” (Dec 9, 2025)

- [8] CNBC, “Consumer stocks are underperforming. This one looks like it's ready to bounce” (Oct 8, 2025)

- [9] Forbes, “Home Depot Or Lowe’s: The Better Buy?” (Aug 25, 2025)

- [10] CNBC, “Can Home Depot's AI-powered push to court pros move the needle in its own business?” (Jan 16, 2026)

- [11] CNBC, “Contractor survey shows tradesmen feel pretty good — an encouraging sign for Home Depot” (May 6, 2025)

- [14] Reuters, “Amid ICE raids, some Home Depot investors want to know how law enforcement uses its surveillance data” (Jan 16, 2026)