Housing Market Slump and High Rates Weigh on Big-Ticket Demand at Home Depot (The) (HD)

Home Depot (The) is down for 2026 even as it approaches a long seasonal stretch that has historically favored gains, giving traders a fresh lens on the home improvement leader’s next phase.

Key takeaways

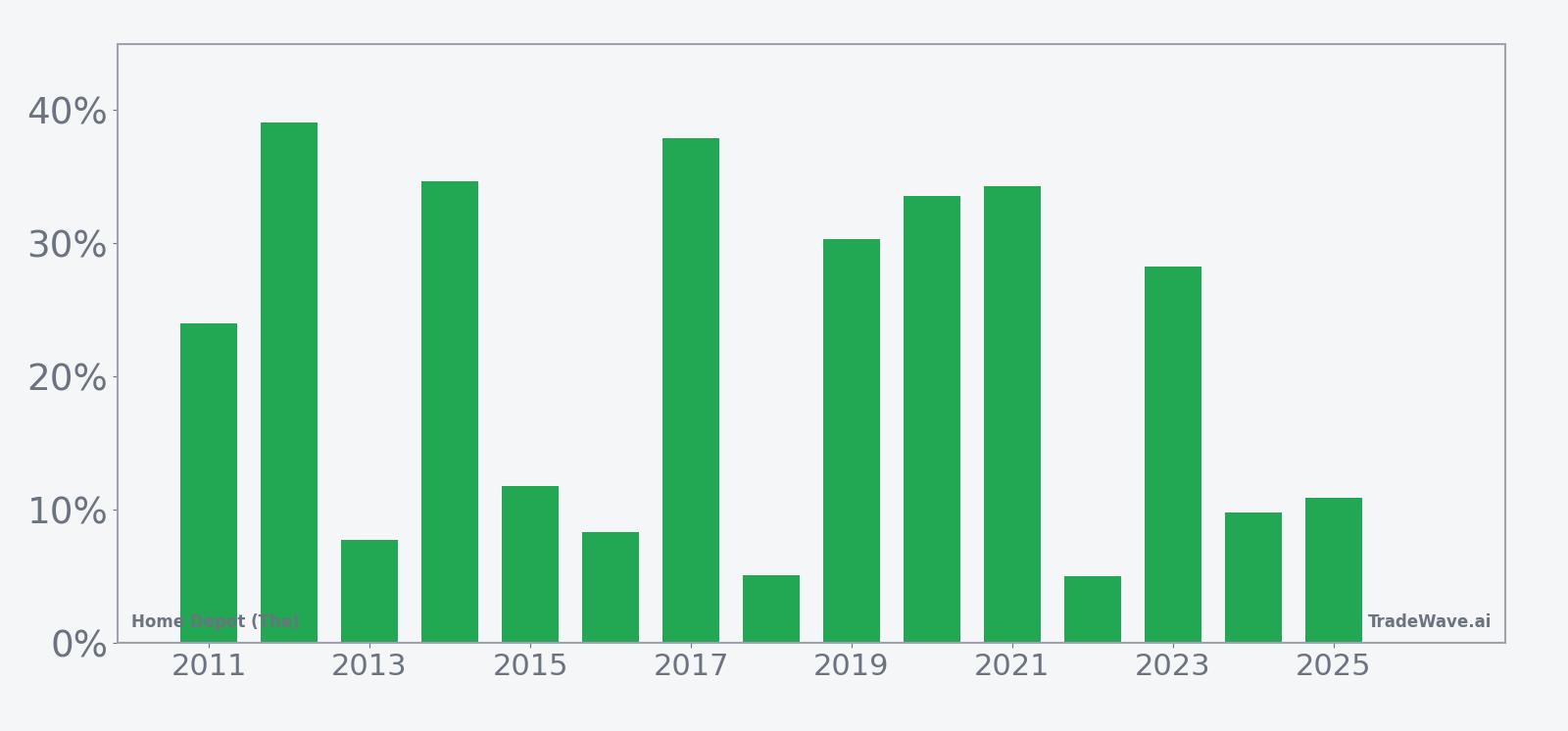

- Home Depot (The) enters a 326-day seasonal window starting Mar 13 that has historically been strongly positive for long positions.

- Across the past 15 years, this window was profitable in 100% of cases, with 15 winners and 0 losers.

- Average profit in winning years was 21.39%, with a median gain of 24.02% over the window.

- The pattern shows sizable upside swings, reflected in a TradeWave Ratio of 1.94 and a Sharpe ratio of 1.35.

- Intraperiod moves have included both sharp rallies and meaningful drawdowns, particularly in years like 2020 and 2022.

- The seasonal backdrop arrives as HD trades lower year to date and digests mixed housing and consumer spending trends.

According to historical data from TradeWave.ai, the coming months line up with one of Home Depot (The)’s most distinctive long-term seasonal regimes. The next section looks at how that pattern has behaved in prior years and how it frames the current setup.

Seasonal window

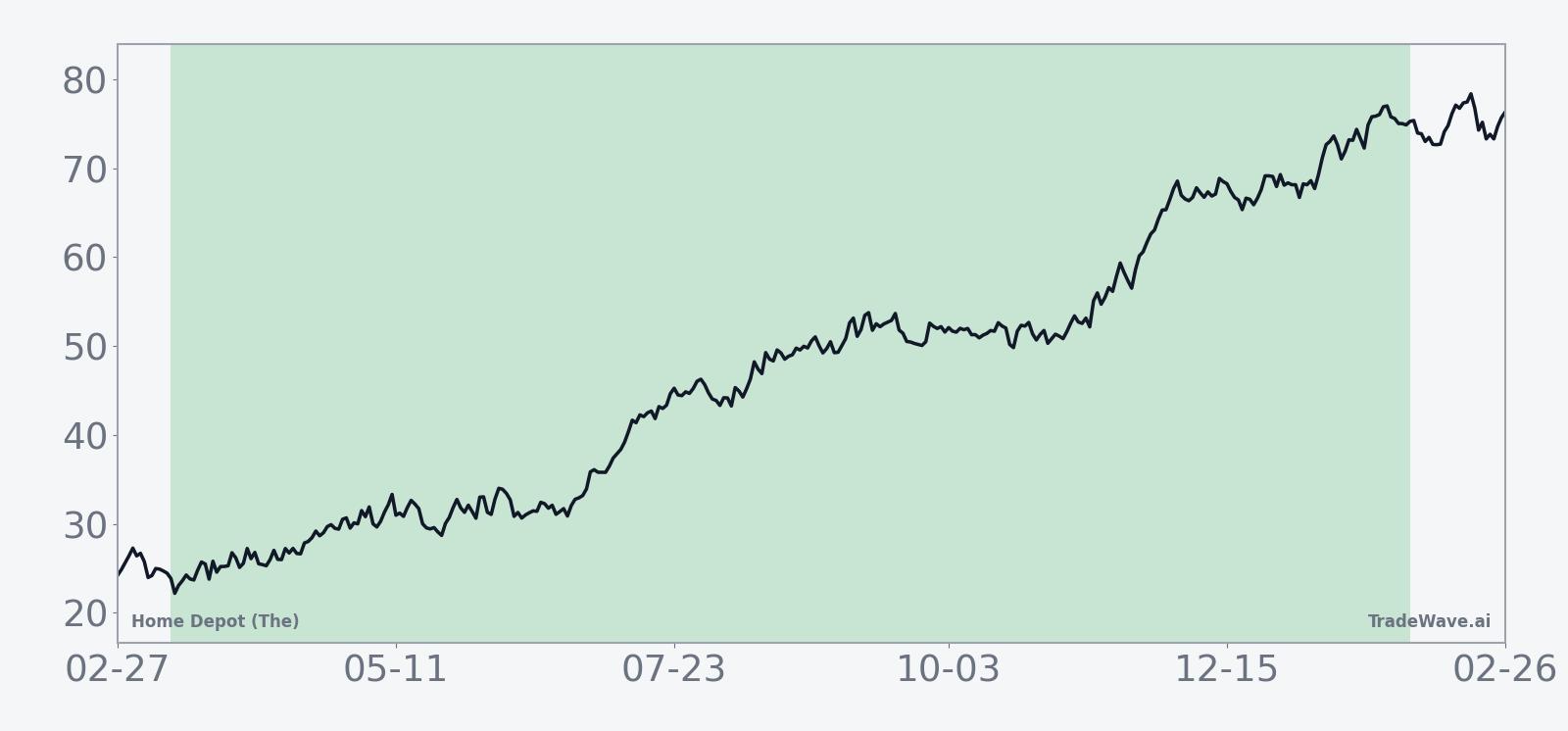

This seasonal window begins on Mar 13, 2026 and spans 326 trading days. Today the stock closed at $375.09, leaving it about 11.7% below its 52-week high of $425 and down roughly 8% for 2026 so far.[6][7]

Historically, this long window has been a strong stretch for Home Depot (The) when traded in the long direction. Across the 15-year sample, every instance finished with a positive net return, with average gains of 21.39% and a median outcome of 24.02%. The cumulative return across all years is 1,584%, which reflects how consistently the pattern has added up over time.

The per-year breakdown shows that some of the strongest outcomes came in 2017, 2019, 2020 and 2021, when net returns ranged from roughly 30% to more than 37%. In 2017, for example, the stock gained 37.88% over the window, while in 2021 it advanced 34.29%. Even the softer years, such as 2016, 2018 and 2022, still finished with single-digit gains, which is why there are no losing years in this sample.

The historical seasonal average suggests that gains tend to build gradually rather than in a single burst. The trend line slopes higher across much of the window, with periods of consolidation and pullback but a clear upward bias overall. That profile is consistent with a long-duration regime where multiple rallies contribute to the final result.

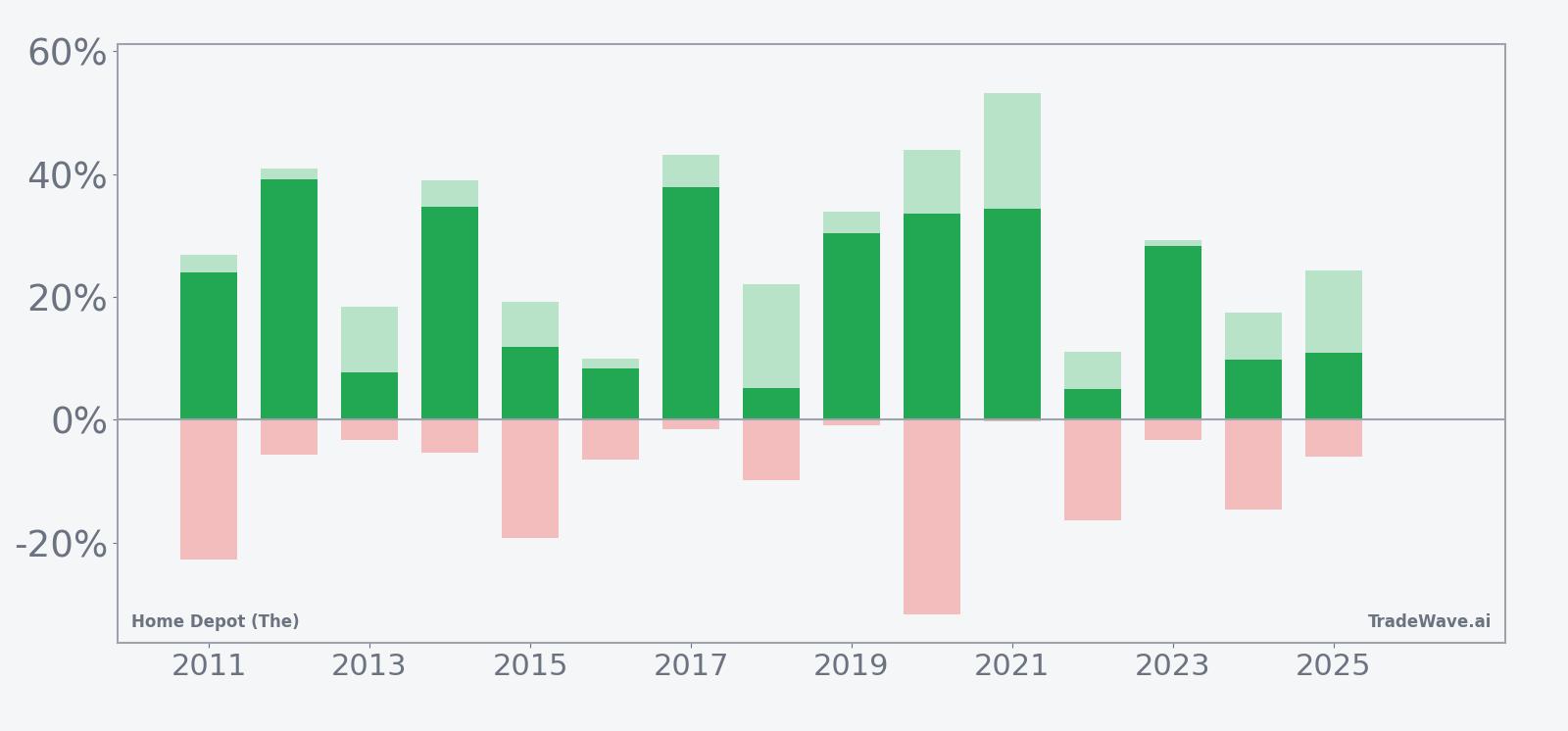

Year-by-year net returns and intraperiod swings highlight how upside and downside have interacted within this window.

The combined net, peak favorable move and worst drawdown chart shows that upside potential has often come with meaningful volatility. In 2020, for instance, the maximum favorable move reached 43.9% while the worst intraperiod drawdown was -31.62%, illustrating a year where the stock ultimately finished higher but experienced a deep setback along the way. By contrast, years like 2017, 2019 and 2021 paired strong maximum favorable moves above 33% with relatively contained worst drawdowns of less than about -2%, highlighting windows where the upside developed with limited adverse pressure.

Other years, such as 2018, 2022 and 2024, show more modest net gains but still feature double-digit peak favorable moves and mid-teens worst drawdowns. That mix underlines that even in a historically strong regime, the path has not always been smooth, and timing within the window has mattered for realized experience.

History does not guarantee future results, and worst-case intraperiod drawdowns can be large even in windows that ultimately finish higher.

Taken together, the historical pattern defines the quantitative seasonal backdrop for the period that begins in mid-March and runs deep into 2027.

Price and near-term drivers

Home Depot (The) shares slipped 0.13% on Friday to close at $375.09, extending a year-to-date decline of about 8% as investors reassess the home improvement outlook after earnings.[6][7] The stock remains below its 52-week high of $425, reflecting a market that is still digesting slower big-ticket spending and a more cautious consumer backdrop.

The latest quarterly report on Feb 24 offered a mixed but generally constructive snapshot. Home Depot posted fourth-quarter earnings of $2.72 per share, topping estimates of $2.54, on revenue of $38.20 billion versus expectations of $38.12 billion, helped by resilient demand from professional customers even as do-it-yourself traffic stayed under pressure.[6][7] Management reiterated that consumers are prioritizing repair and upkeep over large remodels, a shift that has pushed the company to lean harder into pros and smaller-ticket projects.

That message followed a more cautious tone in late 2025. In November 2025, Home Depot reported third-quarter earnings of $3.74 per share, missing forecasts of $3.84, and cut its full-year outlook as a weak housing market and a lack of storm-related repair work weighed on sales.[1][3] At the time, executives guided to a 5% drop in full-year adjusted EPS, with only slightly positive same-store sales, before projecting a return to modest growth in fiscal 2026, including sales growth of 2.5% to 4.5% and flat to low-single-digit comparable sales gains.[13]

Macro conditions remain a key swing factor. High interest rates and a sluggish housing market have curbed demand for big-ticket home improvement projects, while broader economic worries have made consumers more selective about discretionary spending.[1][3] Industry surveys suggest professional contractors are relatively upbeat, which has helped Home Depot offset some of the softness on the consumer side, but the balance between those two customer groups will be central to how the stock trades into the upcoming seasonal window.[7][12]

Strategically, the company is investing in technology and services aimed at professional customers, including an AI-powered push to streamline ordering and project management, as it looks to deepen relationships with higher-spending tradespeople.[10] Analysts tracked by CNBC Investing Club maintain a Buy rating with a consensus price target around $420, implying upside from current levels if the company can execute on its growth plans and the housing backdrop stabilizes.[10]

The chart below situates the latest move in its recent multi-month context.

Earnings and guidance context

The back-to-back earnings prints from late 2025 and early 2026 frame the tension between near-term headwinds and longer-term growth plans. The third-quarter miss and outlook cut in November underscored how sensitive Home Depot is to housing turnover and weather-driven repair cycles, both of which were unfavorable at that point.[1][3][13] By the fourth quarter, the company had regained some footing, beating on both earnings and revenue as professional demand and cost controls helped offset softer do-it-yourself spending.[6][7]

Looking ahead, management’s guidance for fiscal 2026 calls for a return to modest top-line growth, with sales expected to rise between 2.5% and 4.5% and comparable sales projected to be flat to up 2%. Adjusted EPS is forecast to be flat to 4% higher, suggesting that margin discipline and mix shift toward pros will be important levers.[13] With no formal date yet set for the next earnings release, investors are likely to focus on monthly housing data, rate expectations and any commentary from management at industry conferences as early signposts for whether that guidance remains achievable.

Macro and sector backdrop

Home Depot sits at the intersection of housing, consumer spending and construction activity, all of which have been under strain. Weak housing turnover and elevated mortgage rates have discouraged large renovation projects, while a lack of major storms has reduced demand for emergency repair work that often drives spikes in sales.[1][3] At the same time, rising concerns about the broader economy have made households more cautious about discretionary upgrades, even as they continue to spend on essential maintenance.[3]

Within the retail and home improvement sector, the company has responded by sharpening its focus on professional contractors and lower-cost repair categories. That strategy aims to capture steadier, project-based demand from tradespeople while still serving budget-conscious homeowners who are deferring big remodels.[7] If housing activity stabilizes or improves, the combination of a stronger pro franchise and a recovering do-it-yourself customer could provide a tailwind that interacts with the historically favorable seasonal window.

Valuation and positioning

With the stock trading below its 52-week high and down year to date, the market is balancing Home Depot’s long-term franchise strength against near-term macro and housing uncertainty.[6][7] The consensus Buy rating and $420 price target from CNBC Investing Club suggest that many analysts see room for recovery if the company can deliver on its fiscal 2026 growth plan and if rate pressures on housing begin to ease.[10]

For investors who track seasonality alongside fundamentals, the upcoming 326-day window offers a distinct historical reference point. The fact that every year in the 15-year sample finished positive in this regime does not remove risk, but it does highlight that, in prior cycles, this stretch has often coincided with periods when the market rewarded Home Depot’s execution and sector positioning.

What to watch as the window approaches

As the Mar 13 start date for the 326-day seasonal window approaches, several markers will help show whether history is rhyming. First, housing and rate data will be critical: signs of stabilizing mortgage rates or improving home sales could support the company’s guidance and align with the historically strong seasonal backdrop.[1][3][13] Second, the stock’s behavior around key levels, including the recent post-earnings range and the 52-week high near $425, will indicate whether investors are willing to lean back into the name as the window opens.[6][7]

Third, upcoming commentary from management on pro demand, consumer traffic and project mix will be important for gauging whether the shift toward professional customers is gaining traction at the pace implied in recent coverage and analyst views.[7][10][12] Finally, traders watching the seasonal pattern will be alert to how early-window volatility unfolds: in prior years, some of the strongest full-window gains still included sizable drawdowns along the way, so the character of any pullbacks after mid-March may help determine how closely this cycle tracks the historical template.

None of these factors guarantees that the 2026–2027 window will match the past 15 years, but together they outline the fundamental and technical checkpoints that will shape how the market responds as Home Depot (The) moves into one of its historically strongest seasonal stretches.

Sources

- [1] Yahoo Finance, "Home Depot stock falls after company cuts full-year outlook as consumers put off home improvement projects" (Nov 18, 2025).

- [3] MarketWatch, "Home Depot’s stock sinks as good weather and housing weakness lead to a profit miss" (Nov 18, 2025).

- [5] Forbes, "Home Depot Or Lowe’s: The Better Buy?" (Aug 25, 2025).

- [6] CNBC, "Stocks making the biggest moves premarket: AMD, Home Depot, Hims & Hers Health, Diamondback Energy and more" (Feb 24, 2026).

- [7] Reuters, "Home Depot beats quarterly sales estimates on demand from professional customers" (Feb 24, 2026).

- [8] CNBC, "Consumer stocks are underperforming. This one looks like it's ready to bounce" (Oct 8, 2025).

- [10] CNBC, "Can Home Depot's AI-powered push to court pros move the needle in its own business?" (Jan 16, 2026).

- [11] Seeking Alpha, "S&P 500: Stay Safe And React - Week Starting 7th April (Technical Analysis) (SP500)" (Apr 6, 2025).

- [12] CNBC, "Contractor survey shows tradesmen feel pretty good — an encouraging sign for Home Depot" (May 6, 2025).

- [13] The Wall Street Journal, "Home Depot Shares Fall as Retailer Gives Guarded Fiscal 2026 Forecast" (Dec 9, 2025).