Apple (AAPL) Rallies on Robust Q4 Earnings, Services Strength and iPhone 17 Outlook

Apple shares trade around $269 as investors look beyond last year’s iPhone 17 and earnings cycle toward a long seasonal window starting in October 2026 that has historically paired strong upside with notable drawdowns.

Key takeaways

- Apple’s next major seasonal window begins on Oct 3, 2026 and runs for 337 trading days, forming a long regime rather than a short tactical setup.

- The pattern is long-directed and has been profitable in 73% of years, with 33 winners and 12 losers across a 45-year history.

- Winning years have shown an average gain of 59.45%, while including all years brings the average outcome down to 39%, underscoring the impact of losing periods.

- Historical maximum favorable moves inside the window have often been very large, but maximum adverse excursions have also been meaningful, pointing to elevated volatility rather than a smooth climb.

- The seasonal trend profile shows strength that tends to build over the life of the window, with some years experiencing sharp early drawdowns before recovering.

- For a mega-cap like Apple, this combination of strong upside tendency and sizable intraperiod swings could matter for broader index volatility as the 2026 window approaches.

According to historical data from TradeWave.ai, Apple’s behavior around the coming October 2026 window has followed a distinct long-biased seasonal pattern in prior years. The next section looks at how that backdrop fits with today’s price, macro and earnings context.

Seasonal window

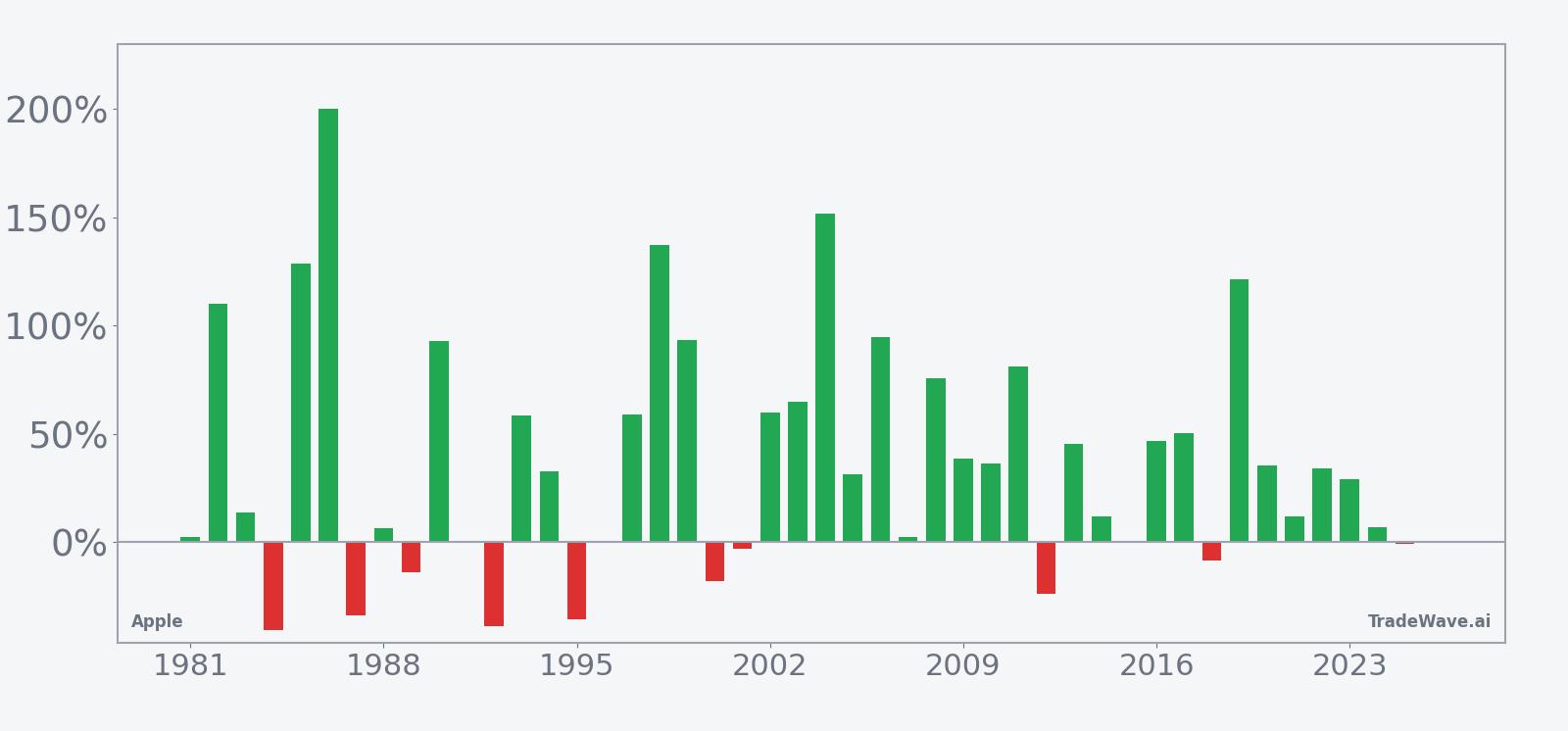

This seasonal window begins on 2026-10-03 and spans 337 days. Historically, during this period, Apple has shown a strong long-directional tendency, with more winning years than losing ones and several very large upside runs inside the window.

Across the 45-year sample, the long trade direction aligns with a clear upside bias: 33 of the 45 windows ended higher, while 12 finished lower, producing a Percent Profitable reading of 73% that reflects the balance of winners and losers. The average gain in winning years was 59.45%, whereas including all years, both positive and negative, brings the average outcome down to 39%, which shows how a minority of losing windows can materially pull down the long-run average.

The per-year history includes standout strong stretches such as 2019, when the window captured a net return of 121.28% with a maximum favorable move of 152.42% and only a modest worst drawdown of 3.2%, as well as more difficult episodes like 2018, when the net result was a loss of 8.46% and the worst intraperiod decline reached 38.6% from the entry level. More recently, the 2024 window still finished positive with a 6.75% gain but experienced a maximum adverse move of 24.85%, illustrating that even ultimately profitable years have seen sizable swings along the way.

The historical seasonal trend chart for this pattern shows a tendency for gains to build over the life of the 337-day window rather than arriving all at once, with the average path grinding higher and occasional periods of consolidation. That profile is consistent with a long regime that often overlaps product cycles and multiple earnings reports, where momentum can accelerate after pullbacks rather than following a straight line.

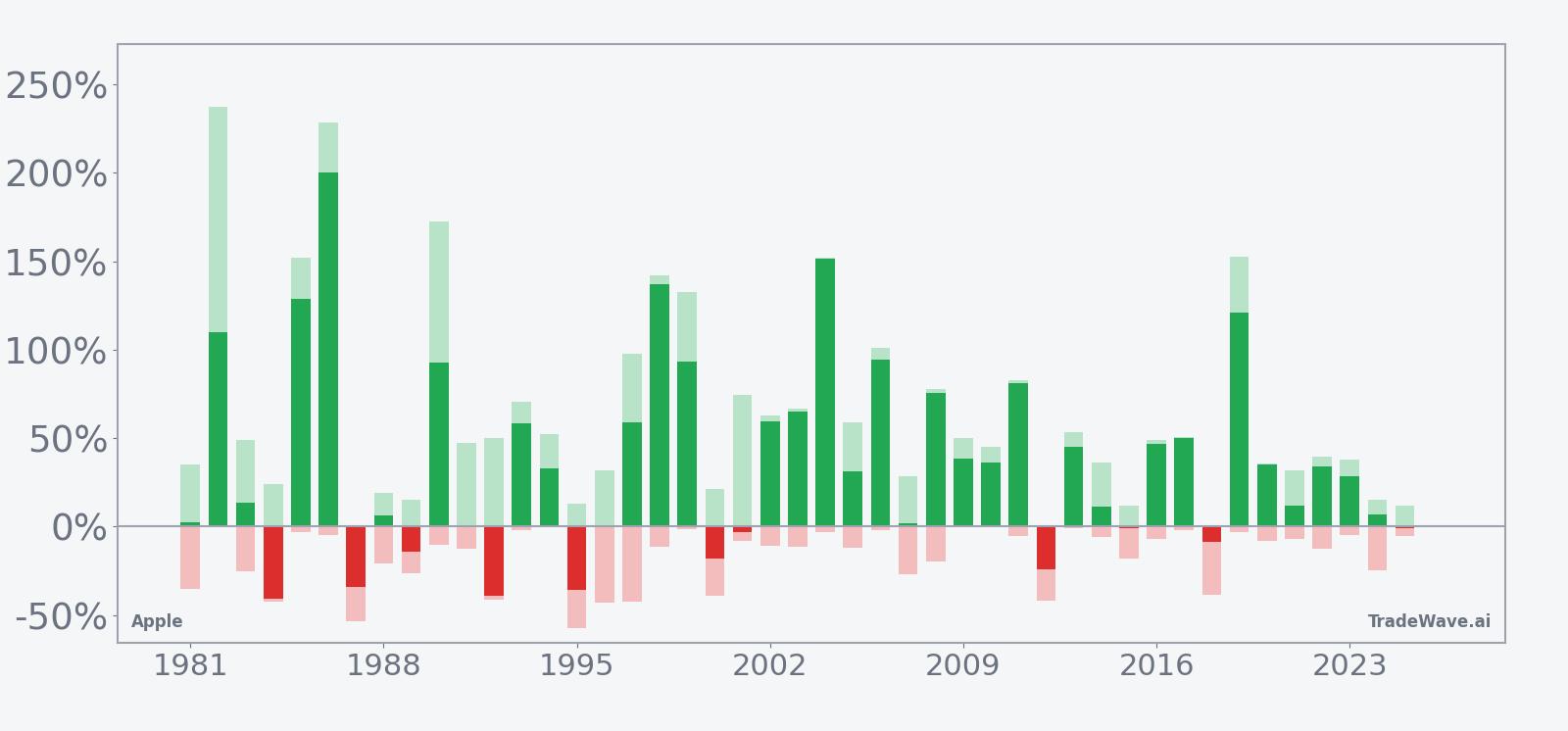

A combined view of net results, peak run-ups and worst drawdowns by year highlights how upside and downside have interacted inside this window.

The combined net, maximum favorable excursion and maximum adverse excursion profile suggests that this upcoming window has historically been both rewarding and volatile: large peak run-ups have often been accompanied by notable drawdowns, and a small set of losing years has been enough to reduce the all-years average despite a strong majority of winners. Taken together, the historical pattern defines the quantitative seasonal backdrop for the period that begins in October 2026.

History does not guarantee future results, and maximum adverse excursions can be large even in winning windows.

Price and near-term drivers

Apple shares last traded at $269.13 on Jan 19, 2026, up 0.34% on the day, leaving the stock without an official year-to-date performance figure in the available data but still reflecting the strong multi-year run that has taken it into the multi-trillion-dollar market-cap club.[3] With no fresh news hooks in the past 60 days, the near-term narrative is still shaped by last year’s iPhone 17 launch and the company’s most recent fiscal 2025 earnings cycle, which helped frame expectations for growth in hardware and services.[3][7]

In Sep 2025, Apple introduced the iPhone 17 lineup, including Pro and Pro Max models, which analysts viewed as a key driver of demand heading into the holiday quarter and a support for the company’s premium pricing strategy.[3] That launch set the stage for Apple’s fiscal fourth-quarter 2025 results, where the company reported revenue of $102.5 billion, up 8% year over year, and diluted earnings per share of $1.85, up 13% year over year, with services revenue reaching an all-time high and management highlighting what it called the best iPhone lineup ever.[7]

Following those results, Chief Executive Tim Cook offered robust guidance on future iPhone 17 sales, which contributed to a post-earnings jump in the stock before some of the initial gains faded in subsequent trading sessions.[7][9] In late 2025, some analysts argued that Apple’s free cash flow trajectory implied the shares could still be undervalued by roughly 20% despite the strong run, while others pointed to a cooling in analyst sentiment after a pair of downgrades, underscoring how views on valuation and growth durability had become more divided.[5][8]

On the Street, Apple carried a Buy consensus rating with a price target around $290 according to Evercore ISI data cited by MarketWatch in Oct 2025, suggesting modest upside from prevailing levels at that time and reflecting confidence in the company’s ability to monetize its installed base and services ecosystem.[1] At the same time, commentary around Apple’s role in artificial intelligence has emphasized both delays in rolling out some AI features and a belief among several analysts that the company could still emerge as an eventual winner in the space as it integrates more on-device intelligence and cloud-based services.[3]

From a positioning standpoint, short interest in Apple stood at about 0.74% of shares as of the latest available data in Nov 2025, a relatively low level that points to limited outright bearish bets against the stock despite the debate over valuation and growth rates.[4] Macro considerations have also remained in focus, with Apple engaged in tariff discussions that could affect pricing and supply chain decisions, particularly for products assembled in China and sold into major markets, adding another layer of uncertainty that investors will weigh alongside the long-term seasonal backdrop.[2]

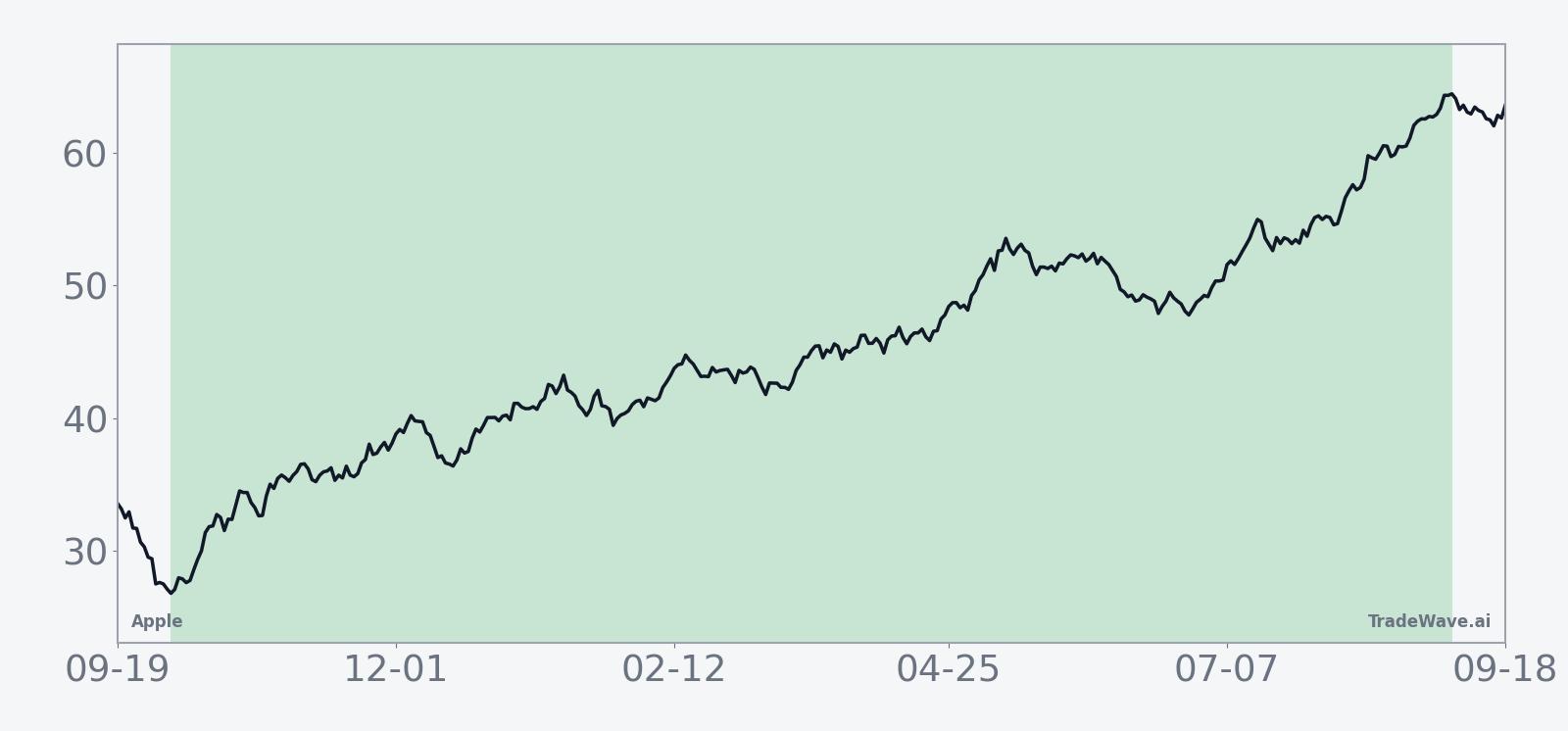

The chart below situates the latest move in its recent multi-month context.

Earnings and fundamental backdrop

Apple’s most recent reported quarter in this dataset is fiscal Q4 2025, where the company delivered mid-single-digit revenue growth and double-digit earnings growth, helped by a richer product mix and continued expansion in high-margin services.[7] Management highlighted record services revenue and strong iPhone performance, reinforcing the narrative that Apple is increasingly a hybrid of hardware and recurring software and services, a mix that can support higher valuation multiples when growth is steady.

Earlier in 2025, investors focused on how Apple would navigate demand trends in China, the trajectory of its services business and the impact of foreign exchange and macro headwinds, with earnings call commentary and analyst notes emphasizing the importance of these factors for the company’s medium-term growth path.[2][6][10] As the 2026 seasonal window approaches, the company is likely to have cycled through additional product refreshes and services launches, which could either reinforce or challenge the historical pattern depending on how those fundamentals evolve.

Macro and sector context

Apple sits at the intersection of several macro themes, including global trade policy, consumer spending and the race to commercialize artificial intelligence. Tariff discussions have periodically raised questions about the cost structure of Apple’s hardware business and the resilience of its supply chain, particularly for iPhone and other flagship devices assembled in Asia and shipped worldwide.[2] Any shifts in tariff regimes or trade agreements over the next year could influence margins and pricing decisions that intersect with the upcoming seasonal window.

Within the broader technology sector, Apple is often grouped with other mega-cap platforms that are investing heavily in AI, even as some analysts have noted that the company’s rollout of certain AI features has lagged more aggressive peers.[3] The prevailing view in late 2025 was that Apple could still be an eventual winner in AI because of its massive installed base and tight integration of hardware, software and services, but the timing and scale of monetization remain open questions that will shape how investors interpret any seasonal tailwinds.

Valuation and expectations

Valuation debates around Apple intensified in 2025 as the stock approached record highs and the company’s market value neared the $4 trillion mark, prompting some analysts to argue that the shares deserved a premium multiple and others to warn that expectations had become stretched.[1][3][5] MarketWatch reported that Evercore ISI’s data showed a Buy consensus rating and a price target around $290, which implied further upside from trading levels at that time but not the kind of deep discount that would typically accompany a contrarian value thesis.[1]

In Nov 2025, Barchart analysis pointed to a surge in Apple’s free cash flow and suggested that the stock could be roughly 20% undervalued, a view that contrasted with the more cautious tone from some other research houses that had downgraded the shares and pushed overall analyst sentiment to a five-year low.[5][8] How those valuation arguments evolve over the next year will influence whether investors see the October 2026 seasonal window as an opportunity to lean into perceived mispricing or as a period to manage risk in a fully valued market leader.

What to watch as the 2026 window approaches

For traders and investors tracking Apple’s long seasonal pattern, the key takeaway is that the 337-day window beginning on Oct 3, 2026 has historically been both strongly positive on average and meaningfully volatile, with 33 winning years and 12 losing years and several episodes of large intraperiod drawdowns. As that date approaches, attention is likely to focus on how upcoming product cycles, particularly any successors to the iPhone 17 family, and the trajectory of services growth line up with the historical tendency for gains to build over the life of the window.[3][7]

In the nearer term, investors may watch for updates on tariff negotiations and supply chain strategy, since changes in trade policy could affect margins and pricing flexibility heading into the seasonal regime.[2] Sector-wide developments in AI will also matter, especially if Apple accelerates its rollout of new AI features or platforms that could alter growth expectations and influence how much weight market participants place on the historical seasonal pattern.[3]

Positioning and sentiment will be another focus point: short interest was relatively low at about 0.74% of shares in late 2025, so any meaningful build-up in bearish bets or a shift in analyst ratings could change the backdrop against which the seasonal window unfolds.[4][5] Finally, traders will likely monitor how Apple trades around future earnings dates and key technical levels in the months leading up to Oct 3, 2026, looking for whether price action aligns with the historical tendency for strong long-directional moves or instead begins to diverge from the established seasonal pattern.

Sources

- [1] MarketWatch, "With Apple stock near a record high as earnings loom, here’s the options trade to make", Oct 20, 2025

- [2] Yahoo Finance, "Q2 2025 Apple Inc Earnings Call", May 2, 2025

- [3] CNBC, "3 reasons Apple deserves its initiation into the $4 trillion club — and what to expect next", Oct 29, 2025

- [4] Seeking Alpha, "Apple plans new features for iPhone satellite services: report", Nov 10, 2025

- [5] Bloomberg, "Apple Analyst Sentiment Hits Five-Year Low After Two Downgrades", Sep 11, 2025

- [6] Business Insider, "Apple earnings updates: Stock rises as Wall Street watches for China sales, services business updates", Jan 30, 2025

- [7] Apple, "Apple reports fourth quarter results", Oct 30, 2025

- [8] Barchart, "Apple's Free Cash Flow Surges, Implying AAPL Stock Could Be 20% Too Cheap", Nov 2, 2025

- [9] CNBC, "Apple gave up its earnings pop. How to trade it from here", Oct 31, 2025

- [10] Seeking Alpha, "Apple expected to report 'good headline numbers' says Wedbush, commentary on iPhone 17 to watch out for", Jul 30, 2025