Microsoft (MSFT) Has Rallied 10 Straight Years in This 160-Day Spring-Summer Window

Microsoft is stepping into a 160-day stretch that has delivered double-digit gains every year for a decade, even as the stock trades well below its 52-week high and investors debate how long the AI boom can keep powering results.

Key takeaways

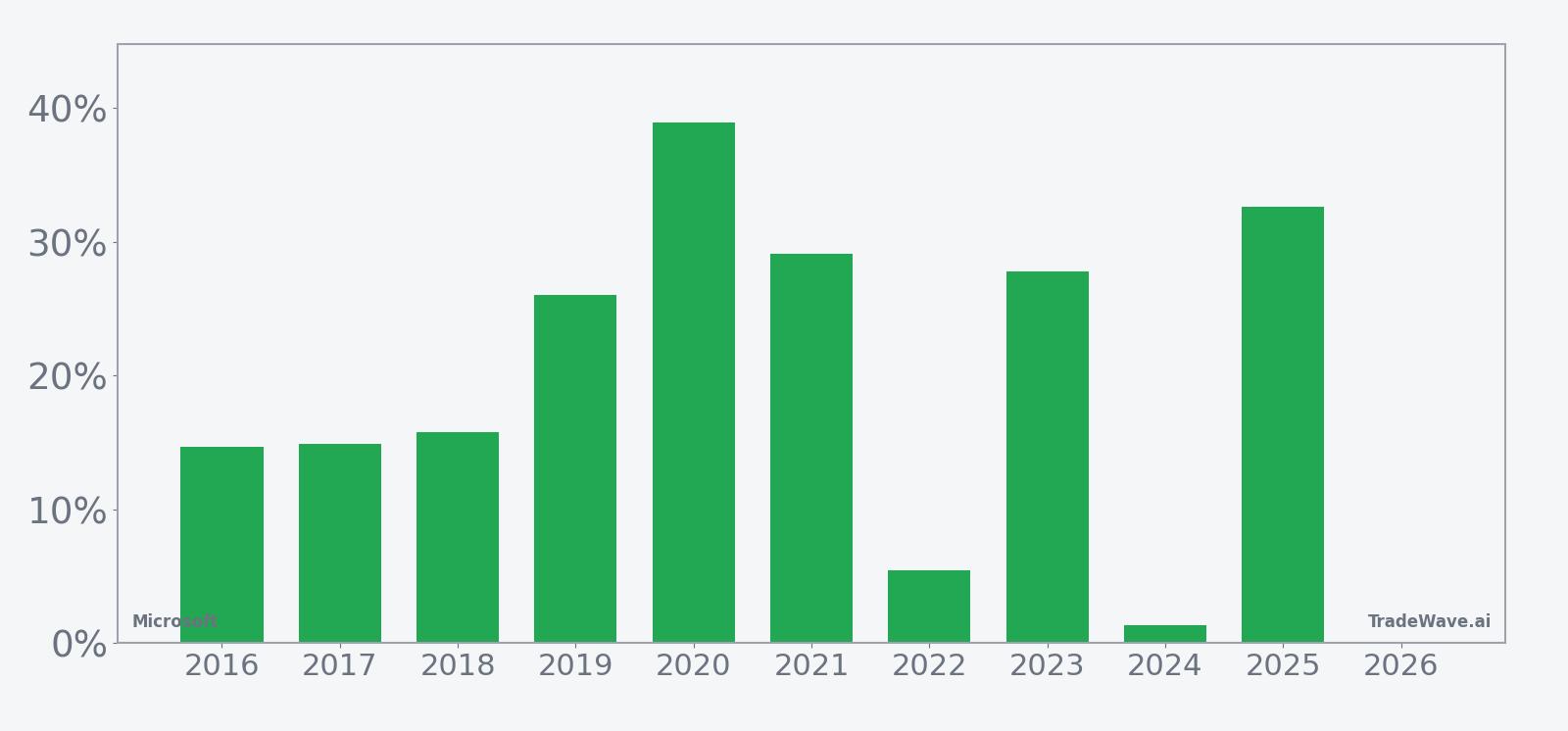

- From Mar 7 over the next 160 trading days, Microsoft has posted gains in 10 of 10 years, a 100% hit rate for this long setup.

- Average profit across those winning windows is 20.67%, with a 524% cumulative return over the decade for this specific stretch.

- Today’s $408.96 close leaves MSFT about 25.5% below its 52-week high near $549, even after a 4.36% gain over the past month.[11]

- Intraperiod swings have been real: in weaker years like 2022, the stock still finished higher but saw adverse moves as deep as about 13% before recovering.

- The pattern’s TradeWave Ratio of 1.94 and Sharpe ratio of 1.56 point to historically strong upside travel relative to risk in this window.

- History shows a tendency for rallies to build over the full 160-day span rather than spike in a single burst, but drawdowns along the way have often been sharp.

According to historical data from TradeWave.ai, this is one of the most consistently positive seasonal stretches on Microsoft’s calendar. The next section unpacks how that pattern has behaved and how it lines up with today’s backdrop.

Seasonal window

Microsoft has risen in 10 of 10 years during this 160-day window starting Mar 7, averaging 20.67% gains for long positions. The stock heads into this year’s iteration at $408.96, about 25.5% below its 52-week high near $549 and modestly higher over the past month.[11] That combination of a clean 10-for-10 seasonal record and a stock trading well off its highs gives this year’s window unusual weight for investors trying to time fresh exposure.

Across the decade, the strongest year in this window was 2020, when Microsoft gained 38.95% between the Mar 7 start and the end of the 160 trading days, while the weakest was 2024 with a still-positive 1.37% net return. Even in softer years like 2022, the stock finished the window up 5.47%, underscoring how consistently this stretch has favored long exposure.

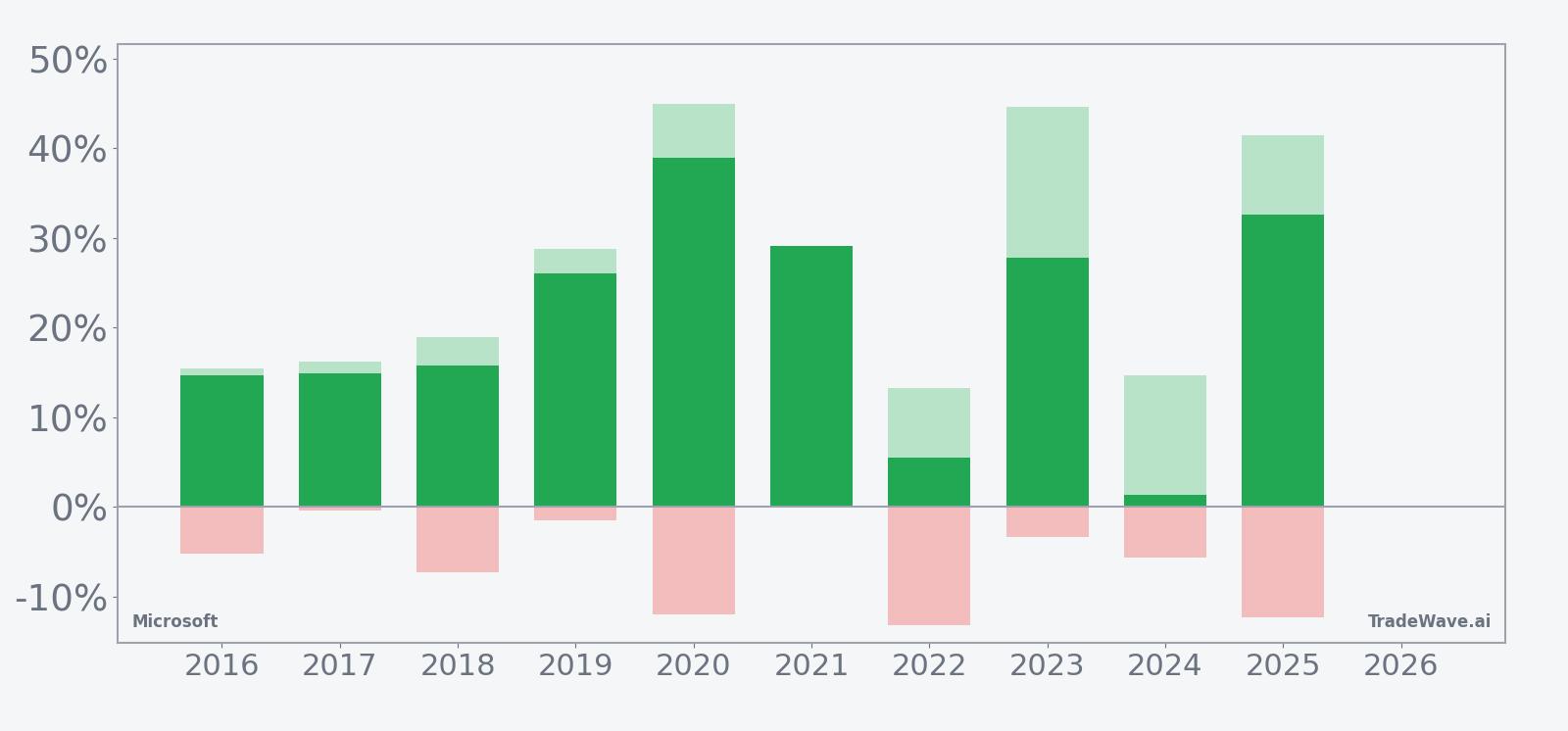

The intraperiod path has not been smooth. In 2020, the best point-to-peak move, or maximum favorable excursion, reached 44.9% before the window closed, while the worst drawdown from entry, or maximum adverse excursion, hit about 12.02% at one point. In 2022, the stock briefly traded roughly 13.21% below the entry level before recovering to a positive finish, showing how this window can combine sizable upside with uncomfortable dips along the way.

Looking across all 10 years, the typical pattern shows gains building over the full 160-day span rather than front-loading in the first few weeks. Years like 2019 and 2025, with net returns of 26.02% and 32.6% respectively, saw Microsoft grind higher with only shallow adverse moves of around 1.44% and 12.34% at worst, while still logging maximum favorable excursions above 28% and 41.48%.

A combined view of net returns with peak run-ups and worst drawdowns highlights how upside and downside have coexisted in this regime.

History does not guarantee future results; adverse excursions can be large even in winning windows, and past 100% success rates can still break.

Price and near-term drivers

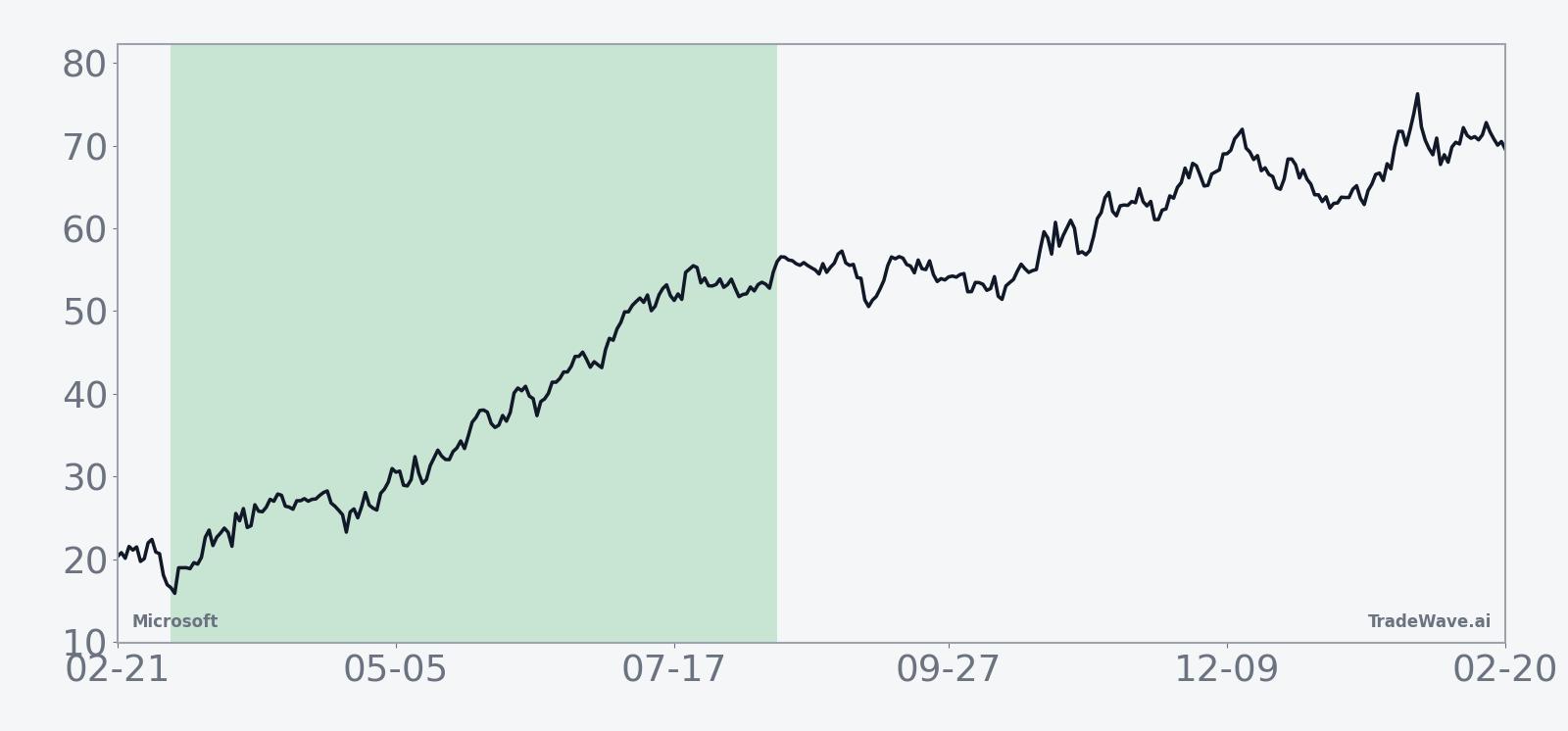

Microsoft closed Friday at $408.96, down 0.4% on the day and roughly 25.5% below its 52-week high near $549, even after a 4.36% gain over the past month as traders rotated back into mega-cap tech.[11] The stock has been digesting a powerful multi-year AI run while investors reassess how much growth is already priced in.

The chart below situates the latest move in its recent multi-month context.

The latest fundamental check came on Jan 28, when Microsoft reported fiscal Q2 results that topped Wall Street estimates but triggered a selloff as investors focused on a slowdown in Azure growth to 39%.[2] Revenue rose 17% year over year and AI-related cloud demand remained strong, yet the market reaction showed how sensitive the stock has become to any hint of deceleration in its core growth engine.

On Jan 30, follow-up analysis highlighted that Microsoft’s commercial remaining performance obligations had climbed to about $625 billion, reflecting a hefty backlog of contracted revenue tied to AI-capable cloud services.[5] That backlog gives the company multi-year visibility on demand, but it also raises the bar for future quarters as investors expect those commitments to translate into sustained double-digit top-line growth.

Fresh commentary in mid February framed Microsoft’s AI positioning as both an opportunity and a source of debate. A Seeking Alpha analysis on Feb 16 argued that questions about “leadership” in AI miss the bigger picture of how deeply the company has embedded AI into its software and cloud stack, while also flagging short interest at just 0.79%, a sign of limited outright bearish positioning in the name.[8] Low short interest can reduce the fuel for sharp squeezes but also signals broad institutional confidence in the long-term story.

More recently, a Mar 4 Forbes piece asked whether Microsoft can keep defying broader market headwinds as AI capital spending and macro worries weigh on sentiment.[11] The article noted that revenue growth over the last twelve months has held near 16.7% despite those concerns, underscoring how resilient the business has been even as the stock has cooled from its highs.

Earnings and guidance

Microsoft’s next scheduled earnings event is its fiscal Q1 2026 report on Oct 29, which will land late in the current seasonal window.[6] That timing matters because several of the strongest historical years in this pattern, including 2019 and 2025, coincided with upbeat earnings that reinforced the underlying trend.

In the most recent quarter, fiscal Q2 2026, revenue increased 17% year over year and Azure grew 39%, both ahead of many expectations, even as the stock sold off on worries that growth was slowing from prior peaks.[2] Earlier, in Q4 2025, Microsoft delivered $76.4 billion in revenue, beating forecasts and briefly pushing its market cap above $4 trillion as investors cheered AI-driven cloud demand.[3]

Management has guided to continued growth from cloud and AI, with Azure expected to surpass $75 billion in revenue as enterprises roll out more AI workloads.[5] That guidance effectively sets the hurdle for the upcoming quarters inside this seasonal window: investors will want to see that AI projects are moving from pilot to production at a pace that justifies the stock’s premium multiple.

Macro and sector backdrop

Microsoft sits at the center of the broader “AI revolution” theme that has dominated equity markets over the past two years. Analysts have argued that AI-driven cloud growth and enterprise deployments could eventually support a $5 trillion market cap for the company, tying its fortunes directly to how quickly AI spending scales across industries.[1]

At the same time, market headwinds have become harder to ignore. A recent Forbes analysis on Mar 4 pointed to concerns that heavy AI capital expenditures and a potential slowdown in global growth could pressure margins and temper investor enthusiasm, even for best-in-class names like Microsoft.[11] That tension between structural AI tailwinds and cyclical macro worries is one reason the stock has stalled below its highs.

Within the technology and cloud sector, Microsoft continues to benefit from strong AI adoption across financials, government and retail customers, which has helped accelerate Azure growth relative to some peers.[1] Another set of Wall Street analysts recently framed the company’s AI integration across software as a key reason they still see meaningful upside for the stock despite a broader “software bear market.”[9]

Valuation and Street positioning

Wall Street remains broadly constructive on Microsoft. Wedbush and other analysts maintain a Buy rating, with a consensus price target around $600 that implies sizable upside from current levels, though some of those targets were set when the stock traded closer to its highs.[1][9] The gap between target and price reflects both confidence in the AI story and recognition that the stock has already rerated higher over the past two years.

Commentary from Forbes in Aug 2025 argued that Microsoft’s strong growth and profitability justified a premium valuation even near $500 per share, framing pullbacks as opportunities for long-term investors.[4] While that view came in a different price regime, the core argument still resonates: as long as AI and cloud growth stay robust, many on the Street are willing to look through near-term volatility.

What to watch in this window

For traders and longer-term investors alike, the next 160 trading days line up as a key test of whether Microsoft’s 10-for-10 seasonal streak can survive a more complicated macro and valuation backdrop. The historical pattern has favored patient longs, with gains often compounding over the full window rather than arriving in a single burst.

Three things stand out to watch. First, Azure and AI growth metrics in the next couple of earnings reports will be critical, especially any signs that enterprise AI deployments are accelerating or stalling relative to the 39% growth pace seen in fiscal Q2 2026.[2] Second, price action around the prior 52-week high near $549 will show whether the stock can reclaim leadership or remains capped by valuation concerns.[11] A decisive move back toward that zone during the window would rhyme with prior strong years like 2019 and 2025.

Third, positioning and sentiment bear monitoring. Short interest remains low at about 0.79%, which means any upside follow-through is more likely to be driven by real money demand than by forced covering.[8] If the stock grinds higher on solid volume while short interest stays muted, it would fit the historical pattern of steady, fundamentals-driven gains in this stretch.

Add it up: Microsoft is entering a seasonal regime that has delivered double-digit gains in every one of the past 10 years, but those gains have often come with sharp drawdowns along the way. How the stock behaves around earnings, key technical levels and AI-related headlines over the coming months will show whether this window remains one of the most reliable spots on the calendar or finally breaks its perfect record.

Sources

- [1] Seeking Alpha, “Microsoft keeps Outperform rating as Wedbush sees 'robust' Q4 results,” Jul 25, 2025.

- [2] Seeking Alpha, “Microsoft stumbles even as Q2 results top estimates,” Jan 28, 2026.

- [3] Business Insider, “Microsoft Stock Surges After It Posts Another Earnings Beat,” Jul 30, 2025.

- [4] Forbes, “Buy MSFT Stock At $500?,” Aug 27, 2025.

- [5] The Motley Fool, “Is It Time to Buy Microsoft Stock as Its Backlog Soars?,” Jan 30, 2026.

- [6] CNBC, “Stocks making the biggest moves after hours: Alphabet, Meta, Starbucks, Microsoft and more,” Oct 29, 2025.

- [8] Seeking Alpha, “Microsoft's Lack Of Leadership In AI, Wait,” Feb 16, 2026.

- [11] Forbes, “Can Microsoft Stock Defy Market Headwinds?,” Mar 4, 2026.