Affordability Pressures, Economic Uncertainty Force Toll Brothers (TOL) to Cut 2025 Deliveries

Toll Brothers has moved into a midterm-election-year stretch that has historically favored downside for the stock, just as shares slip after a strong earnings beat but cautious delivery guidance in a soft housing market.

Key takeaways

- Toll Brothers has entered a 167-day seasonal window starting Feb 18 that, in the last 9 midterm election years, has historically favored a short trade direction.

- The pattern has been profitable in 100% of those years, with 9 winners and 0 losers, and an average profit of 13.32% in the trade direction.

- The TradeWave Ratio of 2.63 suggests price has typically traveled meaningfully in the trade direction within the window, independent of the final close.

- Historical years show sizable peak favorable moves but also notable adverse excursions, indicating that rallies against the short direction have often occurred before the pattern ultimately worked.

- The window is grouped by presidential election cycle, focusing on the last 9 midterm election years rather than consecutive calendar years, which ties the pattern to policy and macro conditions specific to this phase.

- Today’s pullback follows a first-quarter earnings beat and a still-cautious delivery outlook, keeping the interaction between soft housing demand and this historically weak seasonal stretch in focus.[1]

According to historical data from TradeWave.ai, this midterm-election-year stretch for Toll Brothers has shown a distinct seasonal bias that differs from typical calendar-year behavior.

Seasonal window

This seasonal window is currently underway, spanning 167 trading days from Feb 18, 2026, and has historically been a weak stretch for Toll Brothers in midterm election years, favoring a short trade direction. With the stock closing at $159.91 on Feb 18, down 2.4% on the day, investors are watching how this historically soft phase interacts with a name that has already seen volatility around earnings.[1]

Grouping the data by the presidential election cycle matters here because homebuilders are sensitive to policy, rates and fiscal conditions that often shift in midterm years, when Washington typically pivots from early-term agenda setting toward positioning for the next presidential race. By isolating the last 9 midterm election years, the pattern focuses on how Toll Brothers has behaved in comparable policy and macro backdrops rather than averaging across very different parts of the cycle.

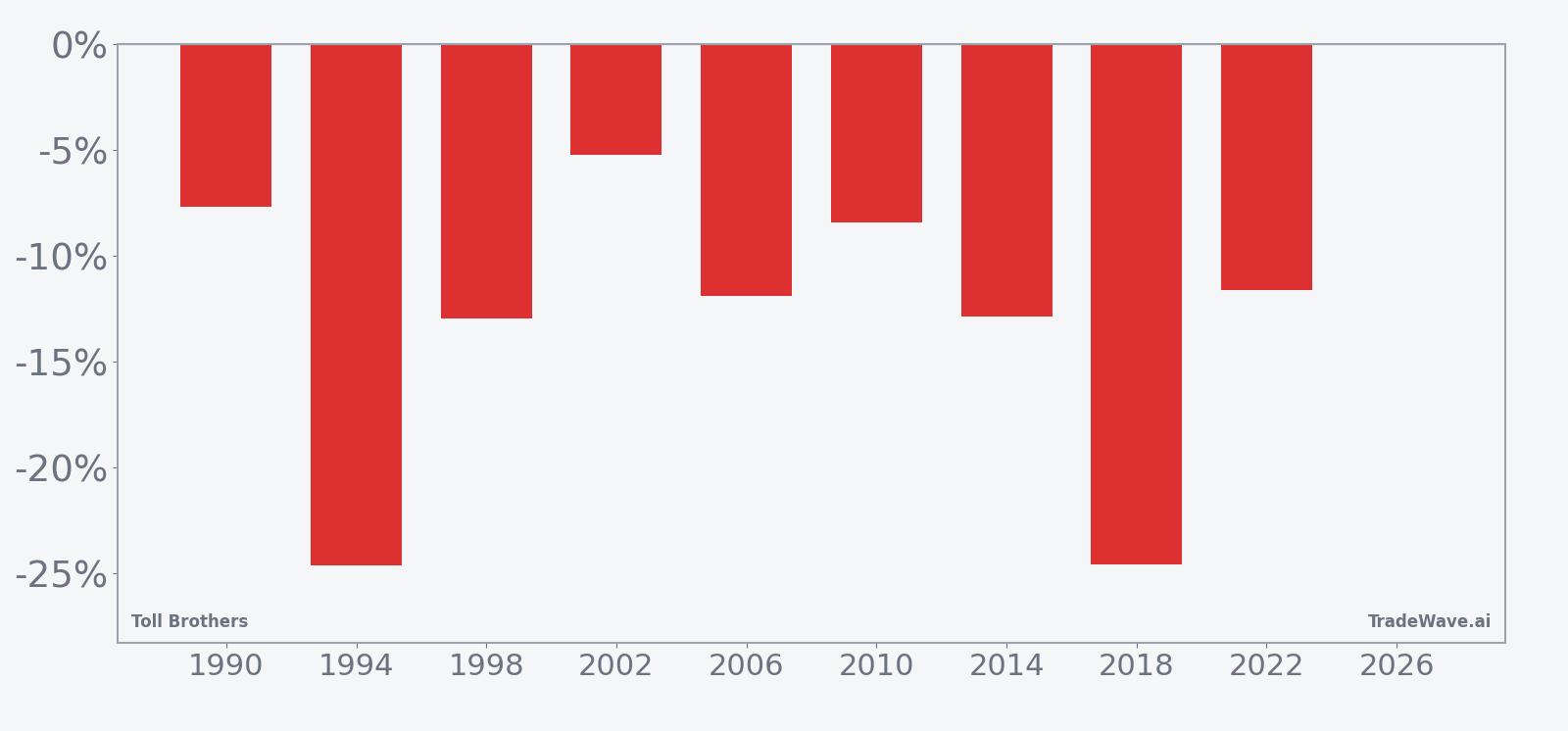

Historically, during this window Toll Brothers has aligned with a short trade direction, meaning the stock has tended to decline over the period in midterm election years. The pattern has been profitable in 100% of the 9 historical instances, with 9 winners and 0 losers for the short setup. Average profit in those winning years is 13.32% in the trade direction, which is sizable for a multi-month window and consistent with the reported cumulative return of 203% across the sample.

The distribution of outcomes is relatively tight for a pattern with a clear directional bias, with a median profit of 11.89% in the trade direction and a reported standard deviation of 6.9%. The Sharpe ratio of 1.67 indicates that, based on end-of-window results, the risk-adjusted performance of this seasonal short pattern has been strong compared with many equity-seasonality setups. The TradeWave Ratio of 2.63 reflects how far price typically travels in the trade direction within the window, regardless of where it finishes, underscoring that intraperiod moves have often been meaningful.

Looking at individual years, the weakest outcome for the short pattern came in 1994, when the net return in the trade direction was 24.62%, meaning the stock fell sharply over the window, while the strongest year for the short setup was 2002, with a more modest 5.22% move in the trade direction. In 2018, another midterm year, the pattern again aligned with a deep decline, with a 24.59% net move in favor of the short direction. These examples illustrate that while the magnitude of the move has varied, the direction has been consistently supportive of the short bias.

The historical seasonal trend chart suggests that weakness for the short pattern has often built gradually rather than in a single shock, with the average path showing a steady move in the trade direction over the life of the window. There are periods of countertrend rallies, but the cumulative effect across years has been a persistent drift that ultimately favors the short side by the end of the regime.

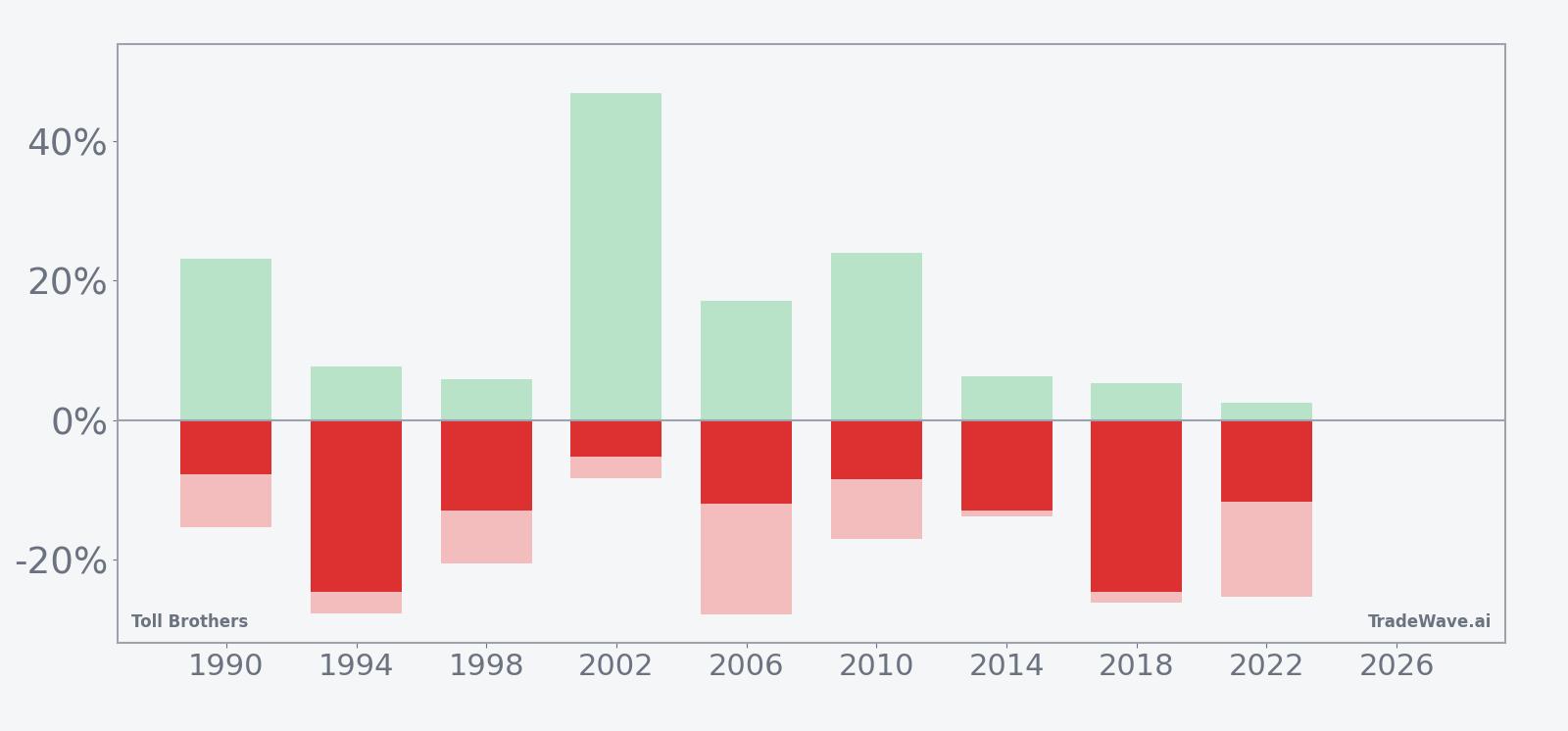

Year-by-year bars that combine net results with peak favorable and adverse moves help clarify how much volatility has typically accompanied this pattern.

The combined net, maximum favorable excursion and maximum adverse excursion bars show that in years like 2002 and 2010, the short pattern ultimately worked but only after sizable rallies against the trade direction, with adverse excursions of 8.31% and 17.02% respectively before the move turned in favor of the short. In contrast, years such as 1994 and 2018 saw deep moves in the trade direction with adverse excursions that were also large, highlighting that this window has historically been volatile even when the final outcome favored the short side. Taken together, the historical pattern defines the quantitative seasonal backdrop for the current period.

History does not guarantee future results; adverse excursions can be large even in winning windows, and traders should be prepared for volatility in both directions within the seasonally weak stretch.

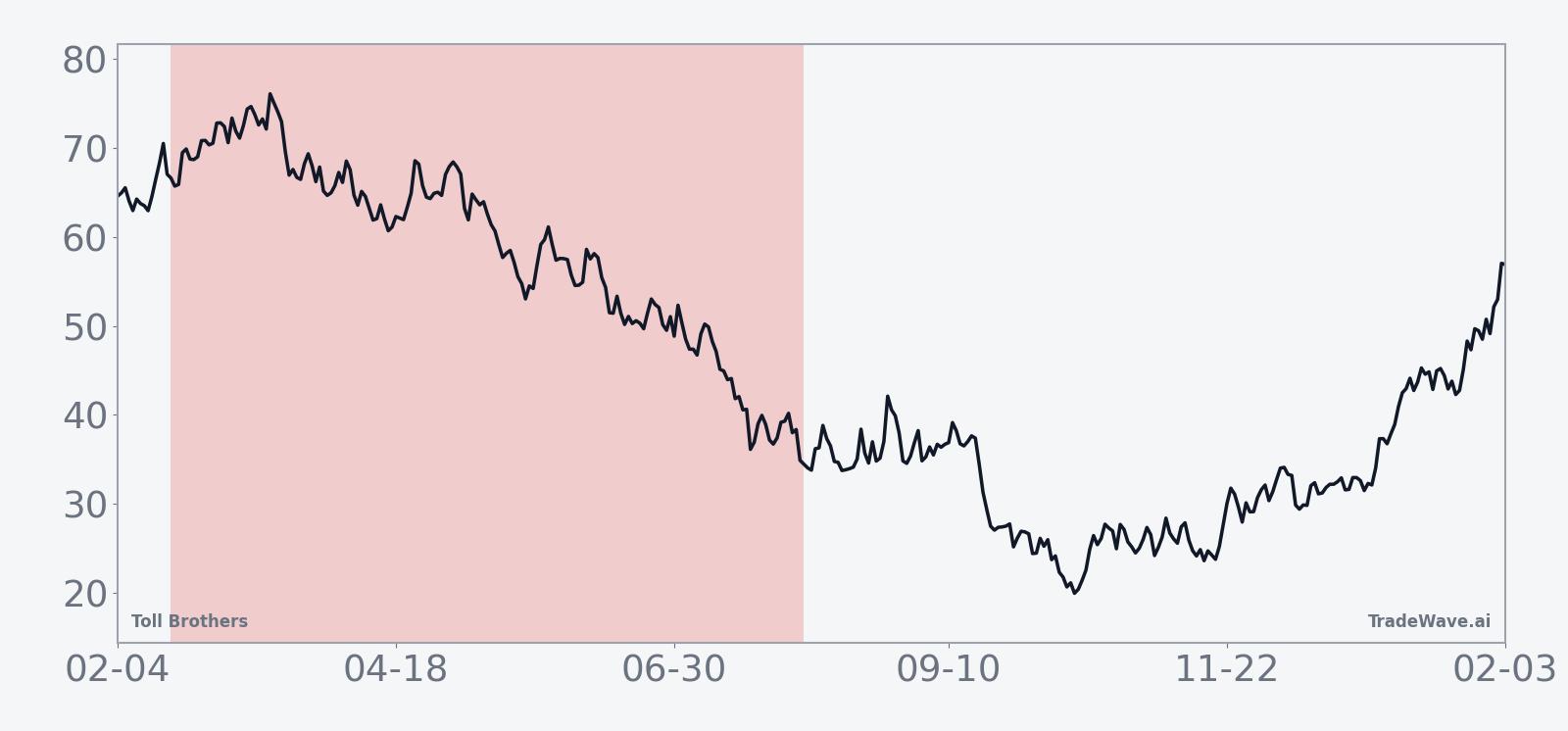

Price and near-term drivers

Toll Brothers shares closed at $159.91 on Feb 18, down 2.4% on the session, as investors digested a first-quarter earnings report that showed stronger revenue but a still-cautious outlook for deliveries.[1] The stock has been trading near record territory in recent months, so even a modest pullback leaves it elevated against the backdrop of a housing market that management describes as soft.

The chart below situates the latest move in its recent multi-month context.

On Feb 17, Toll Brothers reported that first-quarter revenue rose 15% to $2.15 billion, helped by higher land sales, with profit climbing to $210.9 million, or $2.19 per share, topping analyst expectations.[1] The beat underscored the company’s ability to manage pricing and mix even as affordability pressures weigh on parts of the housing market.

At the same time, the company has been cautious about its delivery outlook. In December 2025, Toll Brothers projected fiscal 2026 deliveries of 10,300 to 10,700 units, below analyst expectations of 10,748 units, citing soft housing demand.[2] Earlier, in August 2025, it cut full-year fiscal 2025 delivery guidance to 11,200 units and pointed to affordability pressures and economic uncertainty as key headwinds.[4] Those comments frame the current earnings beat as occurring against a still-fragile demand backdrop.

Sector-wide, homebuilders have been navigating a mixed environment in which higher revenues can coexist with cautious forward guidance, as buyers react to mortgage rates and broader economic signals.[2] For Toll Brothers, which focuses on higher-end homes, the balance between resilient affluent demand and macro uncertainty will be central to how the stock trades inside this historically weak seasonal window.

What to watch in this seasonal window

For the remainder of this 167-day midterm-election-year window, the key question is whether Toll Brothers continues to follow the historical pattern of drifting lower or whether strong fundamentals and earnings resilience offset the seasonal tendency. The pattern’s 100% historical profitability for the short direction and its relatively high TradeWave Ratio suggest that when moves develop, they have often been meaningful, but the sizable adverse excursions in prior years also show that countertrend rallies have been common.

Investors will be watching several catalysts. First, any updates to delivery guidance or commentary on order trends will be important, given management’s earlier caution about 2025 and 2026 volumes and the role of soft housing demand in those outlooks.[2][4] Second, macro data that influence mortgage rates and buyer affordability could either reinforce or challenge the seasonal pattern, particularly if easing financial conditions support higher-end housing demand.

Price-wise, traders are likely to focus on how the stock behaves around recent highs and any emerging support zones on pullbacks. A pattern of lower highs and heavier selling on rallies during this window would be more consistent with the historical short bias, while a sustained break to new highs on strong volume would mark a departure from prior midterm-year behavior.

Finally, because this window sits in the early part of the midterm election year, the evolving policy calendar bears watching. Shifts in fiscal priorities, housing-related regulation or tax policy could alter sentiment toward homebuilders, either amplifying the historical downside tendency or helping the stock resist it. How Toll Brothers trades around these catalysts will show whether the midterm-year seasonal pattern remains a useful backdrop or becomes an exception in this cycle.

Sources

- [1] The Wall Street Journal, “Toll Brothers First-Quarter Revenue Rises Amid Higher Land Sales,” Feb 17, 2026.

- [2] The Wall Street Journal, “Toll Brothers Gives Cautious 2026 Outlook as Housing Demand Remains Soft,” Dec 8, 2025.

- [4] The Wall Street Journal, “Toll Brothers Pulls Back on Home Deliveries Outlook,” Aug 19, 2025.