W. R. Berkley Corporation (WRB) Q2 Profit Climbs on Strong Underwriting, Investment Gains

W. R. Berkley Corporation is approaching a midterm-election-year stretch that has delivered steady gains in the past, giving investors a structured backdrop as they weigh the insurer’s next phase.

Key takeaways

- W. R. Berkley Corporation enters a 129-day seasonal window on Jan 25 that has historically been strongly positive in midterm election years.

- The pattern is based on the last 10 midterm election years, all of which were profitable for a long-direction strategy in this window.

- Across those years, the average profit was 18.91%, with a cumulative return of 429% and a Sharpe ratio of 1.15.

- The window’s TradeWave Ratio of 1.57 indicates that price has typically traveled meaningfully in the trade direction during the period.

- Intraperiod swings have included sizable peak run-ups and occasional drawdowns, underscoring that even a strong seasonal bias can involve volatility.

According to historical data from TradeWave.ai, this upcoming stretch for W. R. Berkley Corporation sits inside a well-defined midterm-election-year pattern that has shown a clear directional tendency in prior cycles.

Seasonal window

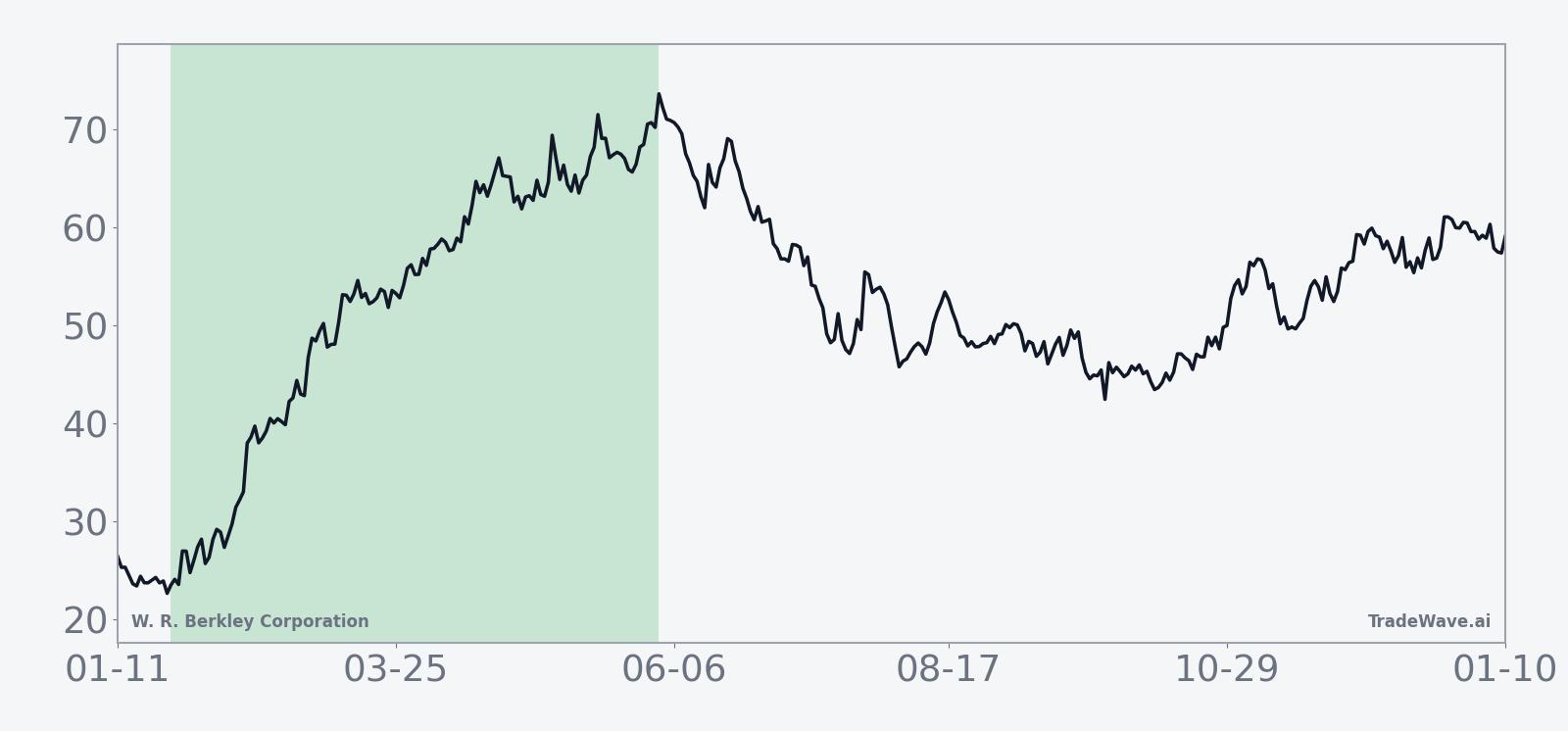

This seasonal window begins on Jan 25, 2026 and spans 129 trading days, and historically it has been a strong period for W. R. Berkley Corporation in midterm election years. With no up-to-date price or 52-week range data available in the current dataset, investors are approaching this window without a precise real-time gauge of where the stock sits versus its recent extremes, which makes the historical pattern a more prominent reference point than usual.

Grouping the data by the presidential election cycle matters here because insurance stocks can be sensitive to policy, regulation and interest-rate expectations, all of which tend to follow a rhythm across the election calendar as Washington shifts focus between campaigning, legislating and implementing new rules.

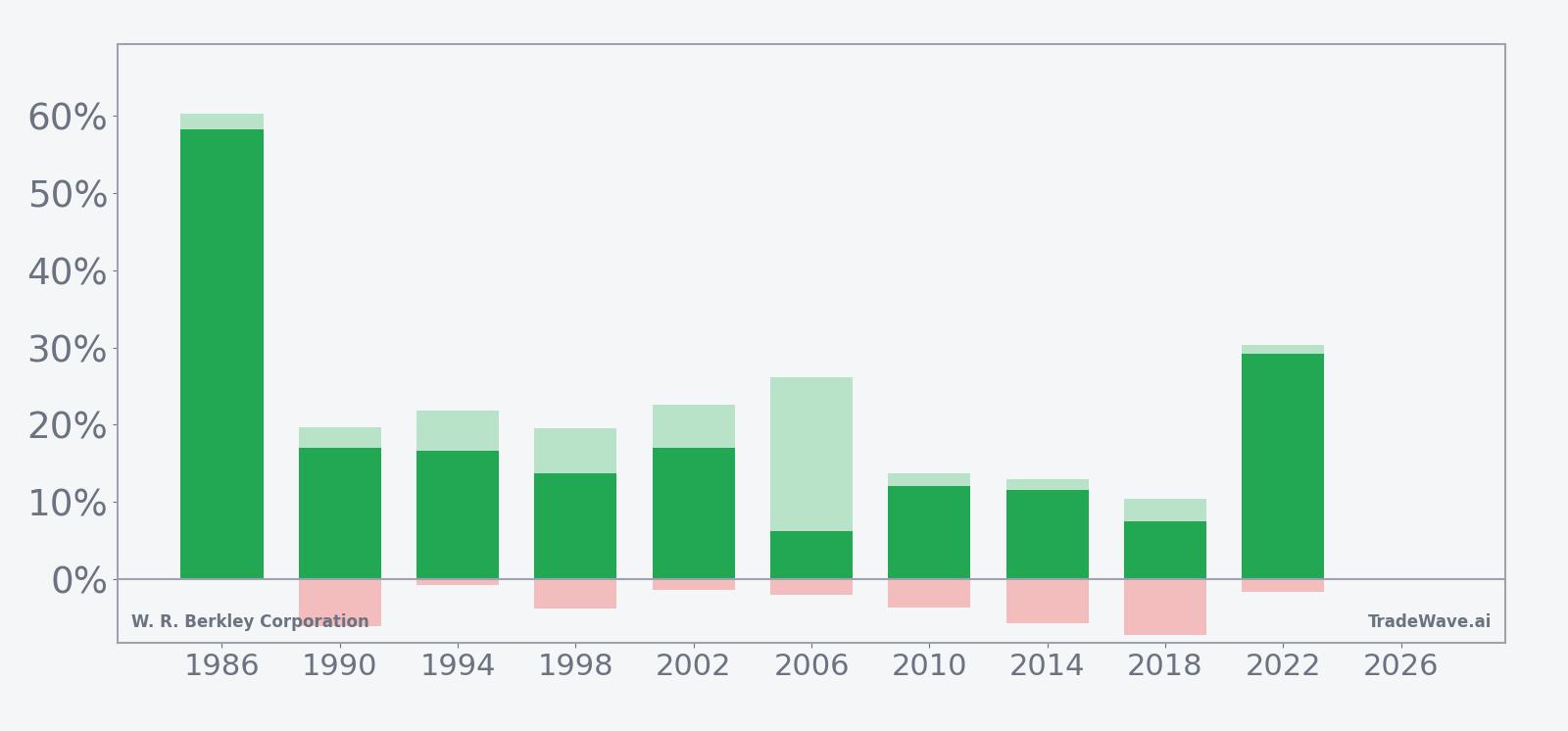

In this case, the pattern phase is defined as “the last 10 midterm election years,” and the trade direction is long. Across those 10 midterm-year instances, the window produced a 100% Percent Profitable record, with 10 winners and 0 losers, meaning every historical occurrence in this sample ended higher over the 129-day span. The average profit across all years was 18.91%, and the cumulative return across the sample was 429%, which points to a consistently constructive backdrop for long exposure during this specific part of the midterm calendar.

The distribution of outcomes shows that the median profit of 15.2% sits somewhat below the average, which reflects a handful of especially strong years pulling the mean higher. The strongest year in the sample was 1986, when the window delivered a net return of 58.15%, while 2022 also stood out with a 29.14% gain. On the softer side of the winners, 2006 posted a 6.26% net return, illustrating that even in a pattern with no losing years, the magnitude of gains has varied meaningfully from cycle to cycle.

Intraperiod behavior has also been constructive. The TradeWave Ratio (TWR) for this pattern is 1.57, which means that price has typically traveled a substantial distance in the trade direction within the window, independent of where it ultimately closed. In several years, the maximum favorable move, or best point-to-peak excursion from the entry, exceeded the final net gain, such as in 2006, when the maximum favorable excursion reached 26.13% even though the final net return was 6.26%.

At the same time, the historical record shows that investors have had to tolerate some downside volatility along the way. The maximum adverse move, defined as the worst drawdown from the entry during the window, reached as deep as -7.19% in 2018 and -5.99% in 1990, even though both years ultimately finished positive. That mix of sizable peak run-ups and occasional mid-window setbacks is consistent with the pattern’s standard deviation of 15.18%, which signals that returns have not been tightly clustered around the average.

The time profile of the pattern, captured in the seasonal trend view, suggests that gains have tended to build progressively rather than arriving all at once. In several of the stronger years, the stock advanced early in the window and then continued to grind higher, while in others the path was choppier, with early drawdowns followed by a recovery and late-window strength. The cumulative return chart for the pattern reinforces this picture, with the average path sloping upward over the 129 days and relatively few instances of prolonged net weakness inside the window.

A combined view of yearly net returns and intraperiod swings highlights how upside and drawdowns have coexisted within this historically favorable window.

History does not guarantee future results, and adverse excursions can be sizable even in windows that have been profitable in every past instance.

Taken together, the historical pattern defines the quantitative seasonal backdrop for the current period.

Price and near-term drivers

Real-time pricing, 52-week range and volume data for W. R. Berkley Corporation are not included in the current dataset, which means investors are heading into this seasonal window without a precise snapshot of how the stock has traded in the very latest sessions. That places more weight on fundamentals and sector context when interpreting the upcoming pattern.

In Jul 2025, W. R. Berkley reported that second-quarter profit for common stockholders rose to $401.3 million, or $1 per share, from $371.9 million, or 92 cents per share, a year earlier, supported by strong underwriting and higher net written premiums that climbed 7.2% to $3.35 billion.[1] Net investment income increased 1.9% to $379.3 million, underscoring the benefit of higher yields for an insurer with a sizable investment portfolio.[1] Those results highlighted the company’s ability to grow earnings despite a backdrop of frequent natural catastrophes and industry-wide loss pressure.

The sector context has been challenging. In Jul 2025, industry data showed that insurers including W. R. Berkley faced catastrophe losses that were up 10.7% to $99.2 million in the second quarter, reflecting the impact of hurricanes, wildfires and other severe events.[1] That environment has kept attention on underwriting discipline, pricing power and reinsurance strategies, all of which can influence how investors respond to any new information that arrives during the upcoming seasonal window.

Macro conditions also matter for a specialty insurer. In Jul 2025, analysts noted that persistent uncertainty over U.S. trade policies and tariffs had pushed some investors toward domestically focused financials and insurers that are relatively shielded from direct trade-war fallout.[1] For W. R. Berkley, which generates much of its business in the United States, that backdrop can be a modest tailwind if it continues, particularly if interest rates remain supportive of investment income.

The chart below situates W. R. Berkley’s recent trading path over the past year, providing context for how the stock has behaved ahead of the new seasonal phase.

Macro and election-cycle backdrop

The calendar phase for this pattern is the midterm election year, which historically has been a distinct part of the presidential cycle for equities and financials. Early in the midterm year, markets often grapple with policy uncertainty as lawmakers debate fiscal priorities, regulatory initiatives and potential changes to taxation or industry oversight. For insurers, that can translate into shifting expectations around capital requirements, litigation trends and the broader economic environment that shapes demand for coverage.

As the midterm year progresses and attention gradually turns toward the following pre-election year, the policy calendar can become more predictable, with fewer major legislative pushes and more focus on positioning ahead of the next presidential race. For a company like W. R. Berkley, which has historically shown strength in this specific midterm-year window, that transition has often coincided with a period in which investors refocus on company-level fundamentals such as underwriting margins, reserve adequacy and investment returns rather than headline political risk.

What to watch as the window unfolds

For investors tracking W. R. Berkley into this 129-day seasonal window, one focal point will be whether the stock’s actual path resembles the historical pattern of steady gains with intermittent drawdowns. A period of early volatility followed by a sustained grind higher would be consistent with the average seasonal trend, while a prolonged slide or flat performance would mark a departure from the last 10 midterm election years.

Fundamentals will remain central. Any updates on catastrophe losses, pricing conditions or reserve development could influence how closely the stock tracks its historical seasonal profile, particularly if severe weather events or litigation trends diverge from prior years.[1] Investors will also be watching how interest-rate expectations evolve, since changes in yields can affect both investment income and the valuation of insurance balance sheets.

From a policy perspective, the midterm-year calendar means that regulatory headlines, proposed insurance reforms or shifts in financial-sector oversight could emerge as catalysts. If the market perceives the regulatory environment as stable or improving for insurers, that could reinforce the historically constructive seasonal backdrop. Conversely, surprise policy moves that raise capital or compliance costs could weigh on sentiment even within an otherwise favorable window.

Finally, traders may monitor how WRB behaves around key technical levels visible on the recent price chart, such as prior highs, lows or consolidation zones. A pattern of buying interest on pullbacks within the window would align with the historical record of positive outcomes, while repeated failures at resistance or heavy selling on news could signal that this midterm-year instance is breaking from the past. In that sense, the seasonal statistics provide a framework, but the real-time reaction to news, policy and macro data will determine how closely 2026 fits the historical script.

Sources

- [1] Reuters, “W. R. Berkley second-quarter profit rises on strong underwriting,” Jul 21, 2025.

- [2] Forbes, “Unmasking W. R. Berkley: The Overachiever You're Missing,” Apr 16, 2025.