Shifting Consumer Spending and Private-Label Pressure Test Colgate-Palmolive (CL)

Colgate-Palmolive shares are down sharply for the year even after upbeat guidance, just as the stock approaches a 49-day stretch that has tended to favor the bulls.

Key takeaways

- Colgate-Palmolive is set to enter a 49-day seasonal window starting Feb 27 that has historically been favorable for long positions.

- Across the past 10 years, this window has been profitable in 90% of cases, with 9 winners and 1 loser.

- Average gain in winning years has been 4.45%, while the all-years average including the lone loss is 4%.

- The pattern shows meaningful upside swings alongside occasional sharp drawdowns, highlighting a historically active period for the stock.

- The window arrives as CL trades at $95.73 and sits roughly 12% lower year to date, following stronger-than-expected Q4 results and upbeat sales guidance.[2]

According to historical data from TradeWave.ai, this late-February stretch has shown a distinct seasonal bias for Colgate-Palmolive in prior years. The following section looks at how that pattern has behaved and how it fits alongside the company’s current fundamentals.

Seasonal window

This seasonal window begins on Feb 27, 2026 and spans 49 days. Historically, during this period, Colgate-Palmolive has shown a strong upside tendency that aligns with a long trade direction. Today the stock closed at $95.73, up 0.7% on the session, leaving it about 12% lower for 2026 so far, which makes the upcoming window particularly notable as investors weigh whether a historically supportive stretch can intersect with a stock that has been under pressure.[2]

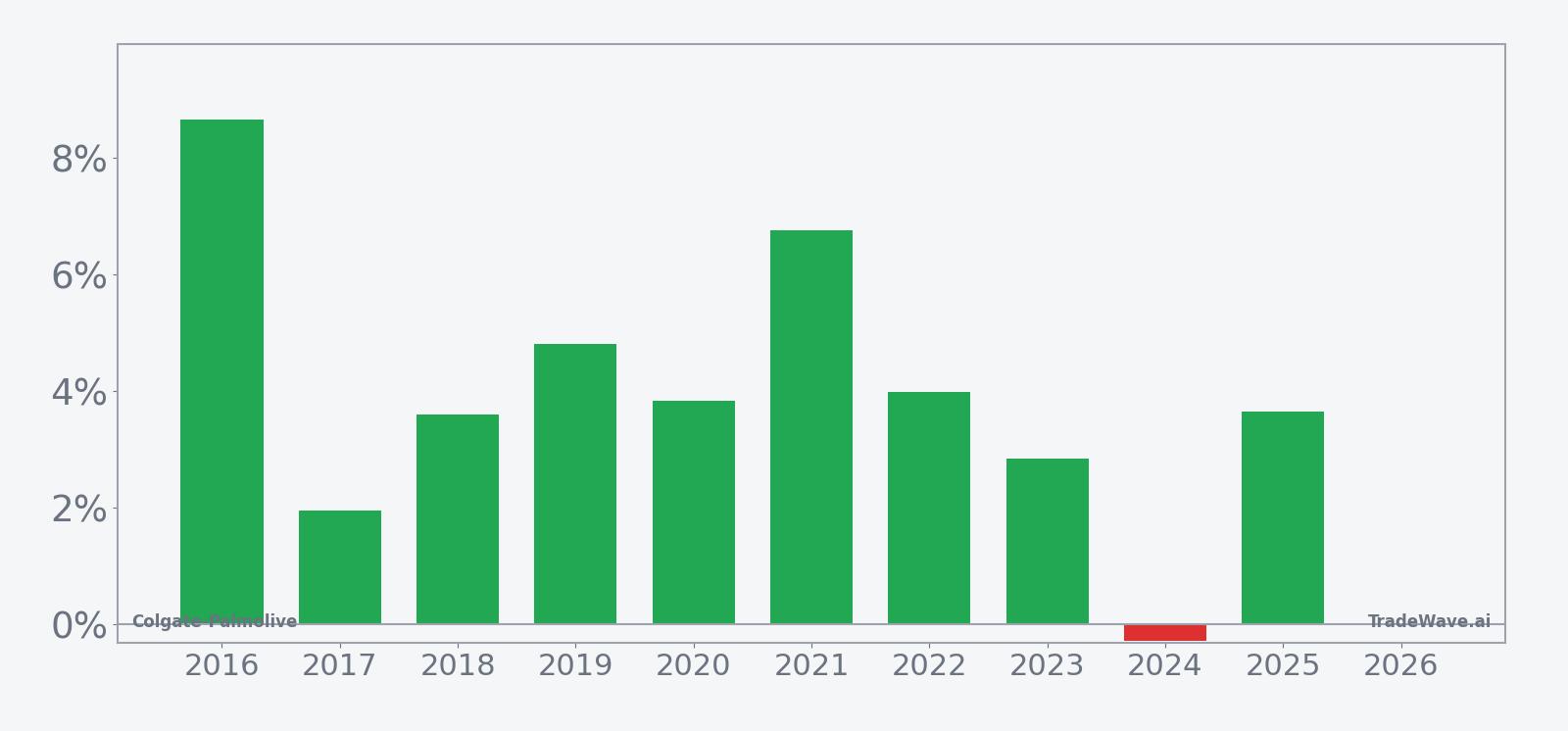

Across the last decade, this 49-day stretch has produced gains in 9 of 10 years, with a Percent Profitable reading of 90%, 9 winners and just 1 losing year. Average profit in the winning years has been 4.45%, while the average outcome across all years, including the lone loss, is a still-solid 4%, underscoring a historically constructive backdrop for long exposure in this period.

The per-year breakdown shows that the strongest outcome in the sample came in 2016, when the stock gained 8.65% between the late-February entry and the end of the window, while the weakest year was 2024, which saw a modest 0.28% decline despite an intraperiod rally that briefly pushed the position into positive territory. That mix of mostly positive closes with one small loss is consistent with the elevated Sharpe ratio of 1.41, which points to relatively strong risk-adjusted returns based on end-of-window results.

The historical seasonal average suggests that gains in this window tend to build gradually rather than in a single burst, with the cumulative return curve rising over the period and only limited stretches of net giveback. That pattern is echoed in the cumulative return statistics, where a 47% total gain across the 10-year sample and a 3.74% median profit point to a tendency for the stock to grind higher more often than not during this part of the calendar.

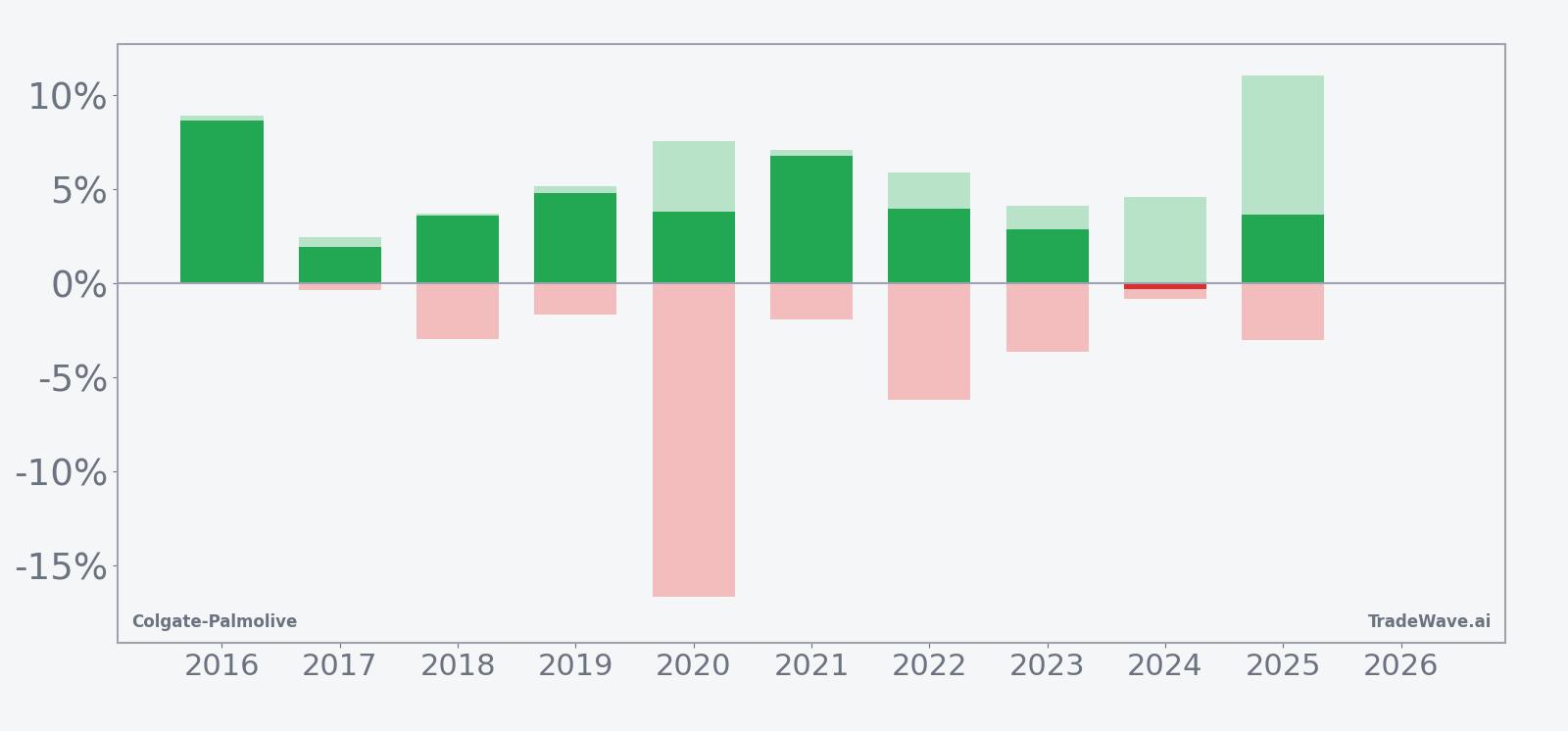

Year-by-year maximum favorable and adverse moves highlight how upside potential and drawdown risk have coexisted in this window.

The maximum favorable and adverse excursions within the window underline that this has been an active period for CL rather than a quiet drift. In 2020, for example, the position finished up 3.83% but experienced a peak run-up of 7.58% and a worst drawdown of 16.62% from entry, while 2025 saw an 11.06% peak gain and a 3.02% worst pullback before closing higher by 3.65%. That combination of sizable intraperiod swings and a long-biased outcome is reflected in the TradeWave Ratio of 2.11, which measures how far price typically travels in the trade direction within the window, and in the 2.45% standard deviation that captures the variability of end-of-window returns.

History does not guarantee future results; adverse excursions (MAE) can be large even in winning windows.

Taken together, the historical pattern defines the quantitative seasonal backdrop for the current period.

Price and near-term drivers

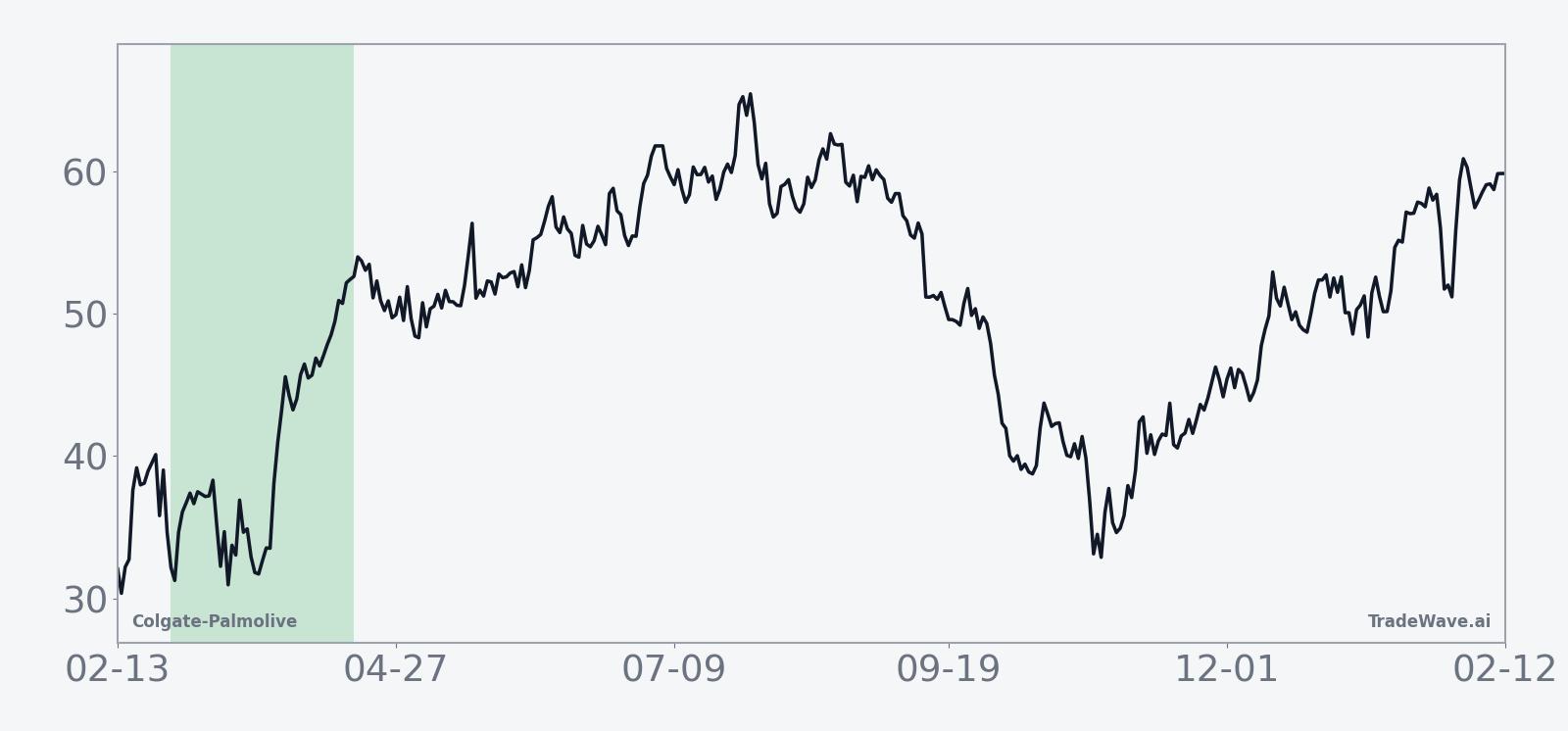

Colgate-Palmolive ended Monday’s session at $95.73, up 0.7% on the day, leaving the consumer-staples heavyweight roughly 12% lower since the start of 2026 as investors reassess growth prospects and valuation.[2] The stock’s pullback comes despite a defensive business mix anchored in oral care and household essentials, which has typically provided some insulation from broader market swings.

The latest leg of the story arrived on Jan 30, when Colgate-Palmolive reported fourth-quarter net sales of $5.23 billion, topping estimates of $5.12 billion, and adjusted earnings of 95 cents per share versus expectations of 91 cents.[2] Management paired the beat with guidance calling for 2026 net sales growth between 2% and 6%, with the midpoint above analysts’ expectations of 3.5%, and reiterated a full-year 2025 outlook for low-single-digit net sales growth, framing the environment as volatile but supported by steady demand for essentials.[2]

Those results built on earlier momentum. In August 2025, the company posted second-quarter profit of $743 million, or 91 cents per share, and revenue of $5.11 billion, both ahead of Wall Street forecasts, while executives highlighted efforts to bolster productivity and manage costs.[3] The combination of cost discipline and modest top-line growth has helped offset some of the pressure from currency and category-specific headwinds.

One of the more persistent drags has been foreign exchange. Adverse currency moves have weighed on reported results, particularly in emerging markets where Colgate-Palmolive has meaningful exposure, even as underlying demand for staples has held up.[1] At the same time, the company has flagged a slowdown in its pet care segment, where post-pandemic inventory adjustments and softer demand have tempered growth, with a more material recovery not expected until 2026.[1]

On the positive side, demand for branded oral care and hygiene products among higher-income households has remained resilient, helping to support pricing and mix even as some middle- and lower-income consumers trade down to private labels.[1][2] That split underscores Colgate-Palmolive’s positioning as both a defensive staple and a brand-driven competitor in categories where shelf space and consumer loyalty still matter.

The chart below situates the latest move in its recent multi-month context.

Earnings and outlook

The most recent quarterly update painted a picture of a company navigating a choppy backdrop with some success. For the fourth quarter of 2025, Colgate-Palmolive’s net sales and adjusted earnings both exceeded consensus forecasts, helped by firm demand in oral care and continued cost control.[2] Management acknowledged a volatile operating environment but emphasized that essentials spending has remained relatively steady, particularly in Latin America and Europe.[2]

Looking ahead, the company expects 2026 net sales growth in a 2% to 6% range, with the midpoint above the 3.5% growth rate analysts had penciled in, and continues to guide to low-single-digit net sales growth for 2025 as a whole.[2] That outlook suggests a modest acceleration from the roughly 2% organic sales growth that some analysts had projected for 2025, even as pet care and foreign exchange remain headwinds.[1][2]

Earlier in 2025, Colgate-Palmolive also delivered a stronger second quarter, with revenue and profit both rising and topping expectations, while executives outlined plans to bolster productivity and streamline operations.[3] Together, the recent quarters point to a company leaning on pricing power, brand strength and efficiency gains to offset softer volumes in certain categories.

Macro and sector backdrop

Colgate-Palmolive’s performance is closely tied to global consumer spending patterns, particularly in everyday staples. While demand for essentials has held up in many markets, the company has noted that middle- and low-income shoppers are increasingly shifting toward private-label alternatives, especially in price-sensitive regions.[1][2] That trend puts a premium on brand equity and innovation in oral care and personal hygiene, where Colgate-Palmolive continues to compete aggressively.

Currency remains a key macro variable. Adverse foreign exchange rates have negatively affected reported sales and earnings, even when local-currency performance has been more stable.[1] For a company with significant exposure to emerging markets, swings in the dollar and local currencies can amplify or dampen underlying trends, and that sensitivity is likely to remain a feature of the story through 2026.

Within the broader consumer-products sector, Colgate-Palmolive faces intense competition but benefits from entrenched positions in oral care and household hygiene, particularly among higher-income consumers who have been less inclined to trade down.[1][2] At the same time, the pet care slowdown illustrates how category-specific cycles can diverge from the core staples narrative, with inventory normalization and changing post-pandemic behavior weighing on that business until a fuller recovery takes hold.[1]

Valuation context

While detailed valuation metrics such as price-to-earnings ratios or dividend yield are not available in the current dataset, the combination of a double-digit year-to-date decline and steady, if modest, growth guidance frames the debate for investors.[2] On one side is a defensive business with resilient demand in key categories and a track record of beating expectations; on the other is a stock that has lagged in early 2026 as markets weigh currency headwinds, pet care softness and competitive pressures.

Against that backdrop, the upcoming seasonal window provides an additional lens rather than a standalone signal. Historically, this part of the calendar has coincided with a constructive period for CL shares, but how that interacts with current earnings expectations and macro conditions will depend on whether management can deliver on its growth and productivity plans.

What to watch as the window opens

As Colgate-Palmolive approaches the Feb 27 start of its historically strong 49-day window, traders and longer-term investors alike will be watching how the stock behaves relative to its recent downtrend.[2] A move that aligns with the historical pattern would likely feature a gradual grind higher with intermittent pullbacks, while a failure to gain traction could signal that current macro and category-specific headwinds are outweighing the usual seasonal tailwind.

Fundamentally, the key checkpoints will be any updates on 2026 sales guidance, particularly around the 2% to 6% growth range, and signs of stabilization or improvement in the pet care segment as the year progresses.[1][2] Currency commentary will also matter, given the role foreign exchange has played in shaping reported results in recent years.[1]

From a price perspective, investors may focus on whether CL can build a base around current levels and start to retrace some of its roughly 12% year-to-date decline during the window, or whether rallies continue to be sold.[2] Intraperiod behavior will be important: historically, even winning years have seen meaningful drawdowns, so the depth and timing of any pullbacks could help gauge whether the pattern is tracking closer to stronger years like 2016 and 2025 or to the lone losing year in 2024.

Ultimately, the seasonal statistics provide a quantitative backdrop rather than a forecast. The interaction between that history, the company’s execution on its earnings plan and the broader macro environment will determine whether this year’s window reinforces Colgate-Palmolive’s reputation as a steady compounder or extends the stock’s early-2026 softness.