AI Power Constraints Cloud Supercycle Hopes for Nvidia (NVDA) After Record Q3

Nvidia shares are under pressure in late February trading even as the stock approaches a historically strong 95-day stretch starting Mar 21, a period that has often coincided with powerful AI-chip rallies.

Seasonal window

Nvidia is heading into a historically strong seasonal window that begins on Mar 21 and runs for 95 trading days, a period that has often aligned with some of the stock’s biggest AI-driven surges. Today the shares closed at $185.37, down 5.2% on the session, leaving the stock well below last year’s peaks and highlighting how volatile the name remains around key inflection points.[8] A large bearish options position established in late February 2025, involving more than 300,000 contracts targeting a drop toward $115, underscored how aggressively some traders have been willing to bet against Nvidia when momentum cools.[13] The combination of a historically favorable seasonal backdrop and a market that has shown it can swing sharply in both directions sets up a high-stakes spring for one of the market’s most influential stocks.

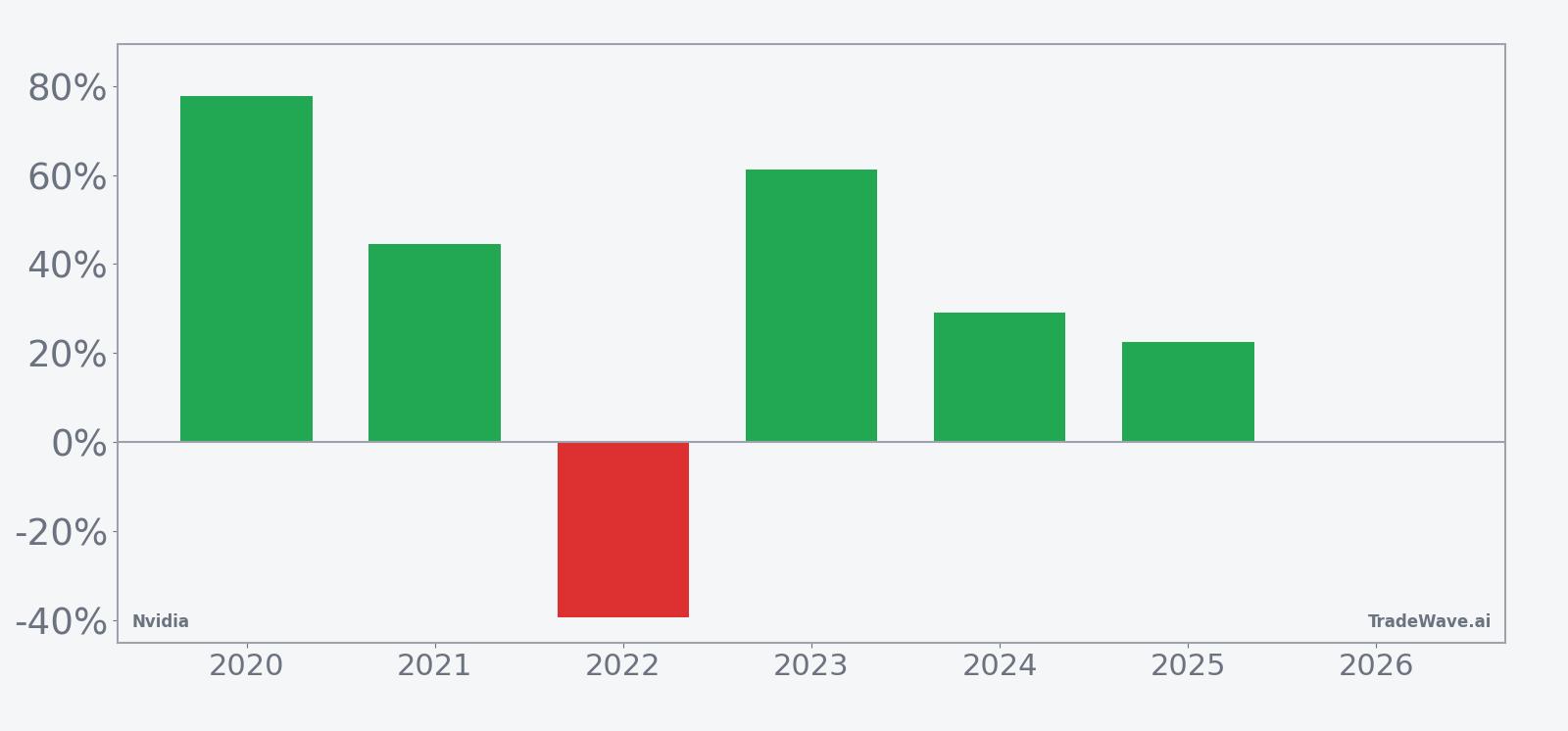

Across the past six years, this 95-day span has been a distinctly bullish regime for Nvidia when viewed through a long trade lens. The pattern has been profitable in 83% of years, with 5 winners and just 1 loser, and the average gain in winning years has been 47.03%, compared with a 33% average when all years are included. That gap reflects the impact of the single losing year, which saw a 39.3% decline, but the overall profile still tilts clearly positive for the period.

The per-year breakdown shows how wide the range of outcomes has been. The strongest year in the sample was 2020, when Nvidia gained 77.8% during the window, while 2022 was the outlier, with a 39.3% loss despite an early attempt to rally. In 2023 the stock advanced 61.13% over the same stretch, and 2024 and 2025 delivered gains of 29.18% and 22.5% respectively, underscoring how often this window has coincided with powerful AI and data-center narratives.

The historical seasonal trend line suggests that, in winning years, much of the upside has tended to accrue steadily across the window rather than in a single burst, with several episodes where rallies accelerated after an initial consolidation. The cumulative return profile, which aggregates these years, points to a pattern where gains often build on themselves once the move is underway, although the 2022 drawdown shows that the path can still be uneven.

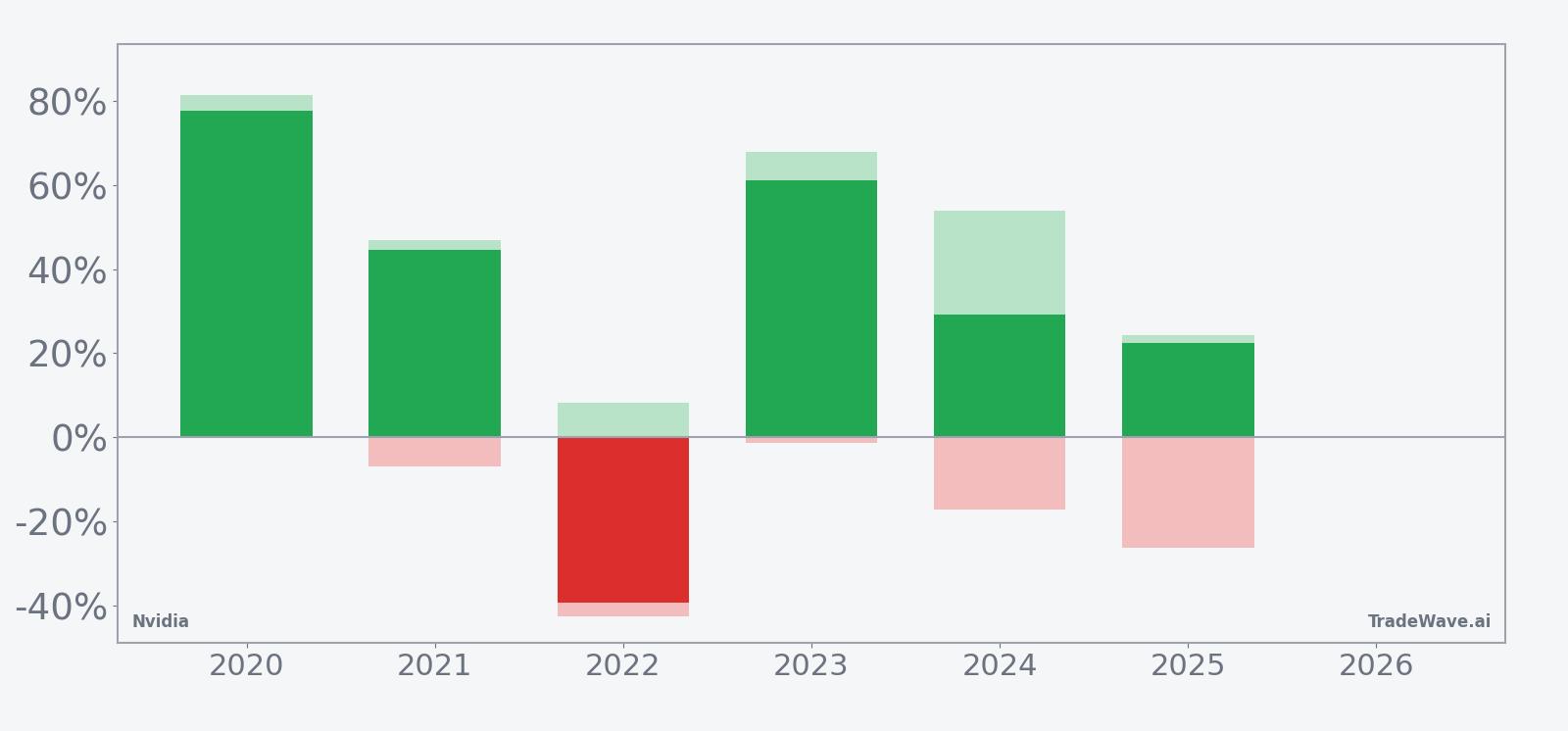

Year-by-year net returns and intraperiod swings highlight how upside and downside have coexisted in this window.

The maximum favorable and adverse excursions within the window underline that this has been a high-energy period for the stock. In 2020, the best point-to-peak move reached 81.43%, while the worst drawdown from entry was limited to 7.22%, a combination that illustrates how strong years can feature large rallies with relatively contained setbacks. By contrast, 2022 saw a modest 8.27% peak run-up before a 42.65% intraperiod drawdown, showing how quickly conditions can reverse even inside a historically positive regime. More recent years such as 2024 and 2025 show a mix of sizable upside potential, with maximum favorable moves of 53.96% and 24.22%, and meaningful downside risk, with adverse excursions of 17.31% and 26.41% respectively.

History does not guarantee future results; adverse excursions (MAE) can be large even in winning windows.

Taken together, the historical pattern defines the quantitative seasonal backdrop for the upcoming period.

Price and near-term drivers

Nvidia closed Thursday at $185.37, down $10.19 on the day, as traders continued to reassess how much AI growth is already reflected in the stock’s valuation.[8] The move extends a broader pullback from last year’s highs and comes against a backdrop where the company’s earnings power and capital spending cycle remain central to sentiment around both the semiconductor sector and the wider equity market.

In Nov 2025, Nvidia reported record fiscal third-quarter revenue of $57 billion, up 62% from a year earlier, with net profit climbing 65% to $32 billion, reinforcing its dominant position in AI accelerators.[4] Management guided for fourth-quarter revenue of $65 billion, ahead of analysts’ expectations of $62 billion, and highlighted that demand for its Blackwell architecture and cloud GPUs continued to outstrip supply.[3] Those results helped cement the view that Nvidia sits at the center of the AI hardware build-out, even as some investors began to question how long such growth rates can be sustained.

Analysts have generally remained constructive on the stock despite bouts of volatility. As of late Oct 2025, HSBC’s consensus compiled by Barchart showed a Buy rating on Nvidia with a price target around $320, reflecting confidence that AI-related demand and new product cycles could support further gains over time.[1] At the same time, other commentators have warned that the stock’s rapid ascent and sensitivity to positioning leave it vulnerable to sharp corrections when expectations reset.[10]

Options activity has periodically amplified those swings. In late Feb 2025, Bloomberg reported that the day’s largest options trade was a bearish bet on Nvidia, with a trader buying more than 300,000 contracts tied to a potential drop toward $115 by early March, a structure that effectively positioned for a double-digit decline from prevailing levels at the time.[13] That episode illustrated how quickly sentiment can flip from enthusiasm to caution in a stock that has become a proxy for the broader AI theme.

Sector and macro narratives continue to frame the debate. Analysts have described Nvidia as the clear leader in AI GPUs, with demand expanding beyond hyperscale cloud providers into enterprises and new verticals, broadening the addressable market for its chips.[1] At the same time, some research has argued that AI adoption, while powerful, is constrained by energy infrastructure and materials, suggesting that the pace of GPU deployment could be uneven as data centers grapple with power and supply-chain bottlenecks.[9]

The chart below situates the latest move in its recent multi-month context.

Earnings and product pipeline context

Nvidia’s most recently reported quarter, fiscal third quarter 2025, underscored how tightly earnings are linked to the AI infrastructure cycle. Revenue of $57 billion exceeded consensus estimates of $55 billion, while net profit of $32 billion reflected strong operating leverage as data-center demand scaled.[4] Chief executive Jensen Huang described Blackwell sales as “off the charts” and noted that cloud GPUs were effectively sold out, language that reinforced the perception of a supply-constrained market.[3]

Looking ahead, the company guided for fourth-quarter revenue of $65 billion, above the $62 billion analysts had penciled in, suggesting that management expected momentum to carry into the end of the fiscal year.[3] That guidance will be a key reference point as investors evaluate how actual results track against expectations and whether growth is decelerating, stabilizing or re-accelerating into the upcoming seasonal window.

Beyond the near-term numbers, the product roadmap remains central to the bull case. Bank of America has highlighted Nvidia’s upcoming Blackwell, Blackwell Ultra and Vera Rubin chips as important drivers of growth in 2026, arguing that successive architectures can extend the company’s performance and efficiency lead in AI accelerators.[3] The timing of those launches relative to the seasonal window could influence how much of any historical pattern is driven by product-cycle news versus broader market factors.

Macro and sector backdrop

Nvidia’s seasonal pattern unfolds against a macro environment where AI is increasingly viewed as a multi-year investment cycle rather than a short-lived fad. Research published in Oct 2025 described AI adoption as a “supercycle,” while cautioning that energy infrastructure and materials constraints could slow the pace of GPU deployment in some regions and data centers.[9] That tension between long-term demand and near-term bottlenecks has been a recurring theme in how investors value Nvidia and its peers.

Within the semiconductor and AI hardware sector, Nvidia has been characterized as the clear leader in high-performance GPUs, with its ecosystem and software stack creating a competitive moat that extends beyond raw chip performance.[1] As more enterprises experiment with generative AI and accelerated computing, the company’s role as a key supplier to cloud providers and large corporates has reinforced its status as a bellwether for the broader AI trade.

Valuation and positioning

Valuation has been a persistent point of debate around Nvidia, particularly after the stock’s powerful run into 2025. Nasdaq’s quantitative analysis in Mar 2025 highlighted the company’s strong growth metrics and profitability, while also noting that the shares were trading at elevated multiples relative to many peers.[8] Subsequent commentary on platforms such as Seeking Alpha has ranged from arguments that the stock’s premium is justified by its dominant position in AI to warnings that investors may be “running out of time to sell” if growth slows or competition intensifies.[10][12]

That divergence in views has contributed to the kind of positioning swings seen in the options market, where large bearish bets have occasionally appeared alongside heavy call buying during rallies.[13] How investors balance those concerns with the historical tendency for the upcoming window to favor long positions will help determine whether seasonality reinforces or challenges prevailing sentiment.

According to historical data from TradeWave.ai, this spring period has shown a distinct seasonal bias for Nvidia in recent years, offering a quantitative backdrop to the current debate over valuation, growth and positioning.

What to watch as the window approaches

With the 95-day seasonal window set to begin on Mar 21, investors will be watching how Nvidia trades into and through that period relative to its historical pattern. One focus will be whether the stock can stabilize after its latest pullback and begin to build the kind of steady advance that has characterized many of the winning years in the sample, or whether volatility remains elevated in a way that resembles 2022’s sharp intraperiod drawdown.

Earnings and guidance will be another key catalyst. As the company reports and updates its outlook for data-center demand, Blackwell and subsequent architectures, traders will be gauging whether revenue and margin trends support the kind of strong performance that has often coincided with this window in the past.[3][4] Any signs that AI spending is slowing or that supply constraints are easing more quickly than expected could influence how closely the stock tracks its historical seasonal tendency.

Options and positioning bear close monitoring as well. The large bearish trade reported in Feb 2025 showed how quickly sentiment can swing when investors question the durability of Nvidia’s rally, and similar episodes of concentrated options activity could again shape short-term price action as the window unfolds.[13] A build-up in downside protection or speculative put buying might signal that traders are bracing for a repeat of the more volatile years in the sample, while a shift toward call-heavy positioning could indicate that investors are leaning into the historical upside bias.

Finally, broader AI and macro headlines will help determine whether this seasonal window reinforces or challenges the prevailing narrative. Strong evidence that AI adoption remains on a multi-year upswing, even in the face of energy and infrastructure constraints, would tend to support the pattern’s bullish history.[1][9] Conversely, any signs of a pause in spending or a more cautious tone from major cloud customers could make the path through this historically strong stretch more uneven than the averages suggest.

Key takeaways

- Nvidia enters a 95-day seasonal window starting Mar 21 that has historically favored long positions, with 5 winning years and 1 losing year across the past six years.

- The pattern has been profitable in 83% of years, with average gains of 47.03% in winners and a 33% average when all years are included, highlighting both strong upside and the impact of a single weak year.

- Intraperiod swings have been large: some years saw maximum favorable moves above 80%, while the worst year recorded an adverse excursion of more than 40%, underscoring meaningful drawdown risk.

- The upcoming window arrives as Nvidia trades well below last year’s highs after a sharp daily drop, even though earnings and product-cycle narratives around AI accelerators remain strong.

- Options markets have shown a willingness to place large bearish bets during past pullbacks, so how positioning evolves into this historically strong stretch will be critical to watch.

Sources

- [1] Barchart.com, "Nvidia Stock Just Got a New Street-High Price Target. Should You Buy NVDA Now?", Oct 27, 2025

- [2] Barchart.com, "Analysts Have High Hopes for Nvidia Ahead of August 27. Should You Buy NVDA Stock Here?", Aug 22, 2025

- [3] Business Insider, "Nvidia earnings updates: Analysts are bullish before Q3 results", Nov 19, 2025

- [4] Reuters, "Nvidia beat may yet stir fear on the Street", Nov 20, 2025

- [5] Bloomberg, "Key Takeaways From Nvidia's Fourth-Quarter Report", Feb 26, 2025

- [6] Yahoo Finance, "Nvidia CEO drops 8 bombshell quotes about its future", Aug 30, 2025

- [7] The Motley Fool, "Should You Buy Nvidia Stock Before May 28? Here's What History Says.", May 8, 2025

- [8] Nasdaq, "NVDA Quantitative Stock Analysis", Mar 11, 2025

- [9] Seeking Alpha, "Nvidia: It's Not A Bubble, It's A Dam", Oct 16, 2025

- [10] Seeking Alpha, "Nvidia: You're Running Out Of Time To Sell", Nov 26, 2025

- [11] Seeking Alpha, "Nvidia stock analyzed amid recent selloff", Mar 8, 2025

- [12] Seeking Alpha, "Nvidia: All-Time High Is In Sight, Upgrade To Strong Buy", Jun 13, 2025

- [13] Bloomberg, "Nvidia Decline to a Five-Month Low Is Day’s Biggest Options Bet", Feb 27, 2025

- [14] Bloomberg, "Nvidia Chart Watchers Brace for More Pain With Dip Buyers at Bay", Mar 5, 2025